Rental Property Reserve Fund Explained for Landlords

- Rey Rey Rodriguez

- 1 day ago

- 8 min read

A rental property reserve fund is a dedicated cash account landlords set aside specifically to cover vacancies, unexpected repairs, and planned capital expenses. In the industry, you will also hear this called a capital reserve account or an operating reserve account, depending on its purpose. Both terms describe the same core discipline: keeping money ready before you need it. Without a reserve fund for rentals, a single HVAC failure or a two-month vacancy can turn a profitable property into a cash flow crisis. This guide breaks down exactly how these funds work, how much to save, and how to manage them without tying up capital you need elsewhere.

What is a rental property reserve fund, and why does it matter?

A rental property reserve fund is a pool of cash held separately from your operating account, reserved exclusively for property-related expenses outside your normal monthly budget. Think of it as the financial equivalent of a spare tire. You do not use it every day, but the moment you need it, nothing else will do.

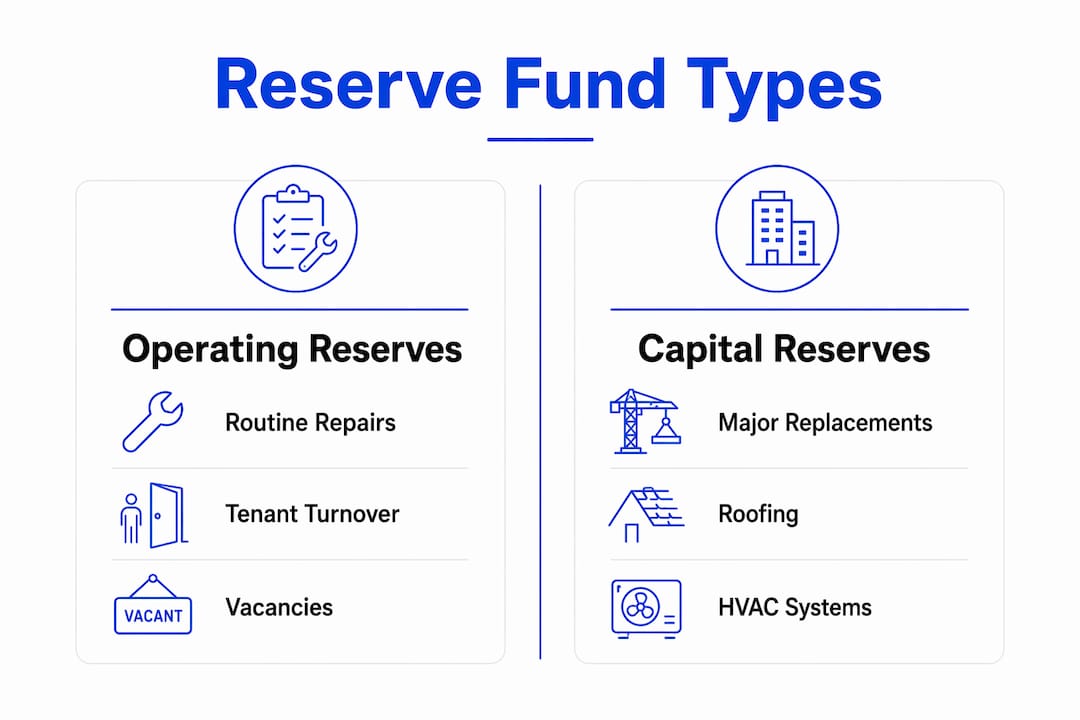

Operating reserves cover routine maintenance, minor repairs, tenant turnover costs, and vacancy periods. Capital reserves address major replacements: roofs, HVAC systems, water heaters, and structural work. Both serve distinct purposes, and confusing them is one of the most common and costly mistakes landlords make.

Keeping reserve funds separate from your operating checking account is not optional if you want accurate financial reporting. When reserves and operating cash share one account, you cannot tell at a glance whether you are truly profitable or just spending future repair money today. Dedicated accounts, whether high-yield savings accounts or separate business checking accounts, give you clarity and a clean paper trail for tax reporting.

The core insight of rental property financial planning is this: a reserve fund does not reduce your returns. It protects them.

What are the main types of reserve funds for rental properties?

Understanding the two primary reserve categories is the foundation of sound property financial planning. They serve different time horizons and expense types, and mixing them creates real problems.

Operating reserves vs. capital reserves

Reserve Type | Purpose | Typical Expenses Covered |

Operating Reserve | Short-term cash buffer for routine costs | Minor repairs, vacancy coverage, tenant turnover, landscaping |

Capital Reserve | Long-term fund for major replacements | Roof replacement, HVAC systems, plumbing overhauls, appliances |

Operating reserves are your first line of defense against month-to-month cash flow disruptions. If a tenant leaves and the unit sits vacant for six weeks, your operating reserve covers the mortgage, insurance, and utilities without forcing you to pull from personal savings.

Capital reserves work on a longer timeline. A roof on a 20-year-old property will need replacement. An HVAC system has a finite lifespan. Replacement reserves fund future wear-and-tear of major components like roofs and HVAC systems and must be kept strictly separate from routine maintenance funds to prevent masking underfunded repairs.

Here is what each fund typically covers:

Operating Reserve Expenses:

Routine maintenance calls (plumbing leaks, appliance repairs)

Lawn care and seasonal upkeep

Vacancy periods between tenants

Tenant turnover cleaning and minor unit prep

Capital Reserve Expenses:

Full roof replacement

HVAC system replacement

Water heater replacement

Major electrical or plumbing system overhauls

Flooring replacement across entire units

Keeping these two funds in separate accounts prevents a scenario where you spend capital reserve money on routine repairs and then face a $15,000 roof replacement with nothing in the account.

How much should you set aside in a reserve fund?

No single number works for every property. The right reserve amount depends on your property’s age, location, local labor costs, lender requirements, and your own risk tolerance. That said, proven benchmarks give you a starting point.

Use the operating expense multiple. Individual rental properties should maintain 3–6 months of operating expenses as reserves. Larger properties or associations typically require 6–12 months. A property with $2,000 in monthly operating expenses needs a minimum $6,000 operating reserve.

Apply the percentage of rent rule for capital reserves. Most investors use rules of thumb like setting aside 5–10% of monthly rent or a fixed $5,000 per property for capital reserves as a starting point. On a property renting for $1,800 per month, that means $90–$180 per month going directly into your capital reserve account.

Use the gross rent percentage method. Setting aside 15–30% of gross rent monthly is a common operating reserve rule of thumb used by experienced investors. This broader figure accounts for both operating and capital reserve contributions combined.

Factor in lender requirements. Effective reserve planning relies on detailed, property-level forecasts that account for asset conditions and specific lender requirements such as six months of PITIA reserves. If you are refinancing or acquiring new debt, your lender may set a minimum reserve floor regardless of your own calculations.

Run a capital expenditure study for older properties. Properties over 15 years old benefit from a detailed forecast that estimates the remaining useful life of every major system. This approach replaces guesswork with a documented funding schedule.

Pro Tip: Review your reserve contributions every January. If you completed a major capital project the prior year, your capital reserve may need a higher monthly contribution to rebuild. If your property is newer with no deferred maintenance, you may be able to hold a leaner reserve without meaningful risk.

The right number is always property-specific. A 1990s duplex in a high-labor-cost market needs a larger capital reserve than a 2018 single-family home in a lower-cost area. Build your reserve around your actual asset, not an industry average.

Why does separating reserve funds protect your financial health?

The most dangerous reserve fund mistake is not underfunding. It is commingling. When operating cash and reserves share one account, you lose the ability to see where you actually stand.

Commingling operating and capital reserves risks masking underfunded major repairs. Clear categorization and property-level documentation are the solution. Here is what proper separation delivers:

Accurate cash flow reporting. You know exactly how much is available for operations versus how much is earmarked for future repairs.

Protection from accidental overspending. Separate reserve accounts prevent accidental overspending and improve clarity on what funds are truly available for each purpose.

Simpler tax reporting. Using dedicated business bank accounts for reserve funds simplifies accounting, eases tax reporting, and adds asset protection layers.

Portfolio-level visibility. Experienced investors track reserves at the property level within a portfolio to avoid a healthy total cash balance masking individual asset liquidity shortages.

That last point is critical for anyone managing more than two or three properties. A portfolio with $40,000 in total cash looks healthy until you realize that $35,000 is concentrated in two properties and a third property has $5,000 against a $12,000 roof replacement due next spring.

Pro Tip: Label each reserve account by property address. If you manage five units, you should have five labeled reserve accounts or at minimum a spreadsheet that tracks reserve balances at the property level. Portfolio-wide totals confuse movement with progress.

For a detailed breakdown of what expenses to plan for, the maintenance cost categories guide from 2ndstreetpropertymanagement covers exactly what belongs in each reserve bucket.

How do you build and maintain a reserve fund over time?

Building a reserve fund is not a one-time event. It is a monthly discipline that adjusts as your property ages and market conditions shift.

Scenario | Monthly Contribution | Target Balance |

New property, low risk | 5% of rent to capital reserve | $5,000 minimum |

Mid-age property (10–15 years) | 8% of rent to capital reserve | $8,000–$12,000 |

Older property (15+ years) | 10–15% of rent to capital reserve | $15,000+ |

Vacancy buffer (all properties) | 1 month of operating expenses | 3–6 months total |

Follow these steps to build a reserve fund that actually holds up:

Open a dedicated account the day you close on a property. Do not wait until you have a repair bill. A high-yield savings account works well for capital reserves because the money sits longer and earns interest. A separate business checking account works better for operating reserves because you need faster access.

Automate monthly transfers. Set a recurring transfer from your operating account to each reserve account on the same day rent is collected. Automation removes the temptation to skip a month when cash flow feels tight.

Document every withdrawal with a category and property address. When you pull from a reserve, record whether it was an operating or capital expense. This documentation protects you at tax time and keeps your reserve balance accurate.

Review and adjust contributions annually. Experts emphasize regular review and adjustment of reserve contributions based on maintenance needs, capital projects, and changing market costs. A property that just had a new roof installed needs less capital reserve funding for the next decade. One with an aging HVAC needs more.

For landlords who want a structured approach to budgeting repair costs, 2ndstreetpropertymanagement has a dedicated guide that pairs well with reserve fund planning.

The best reserve fund approach tailors reserves to each property’s age, location, maintenance history, and lender conditions. No formula replaces knowing your asset.

Key takeaways

A properly funded and separated reserve account is the single most effective tool for protecting rental property cash flow against both routine and major unexpected expenses.

Point | Details |

Two distinct fund types | Keep operating reserves and capital reserves in separate accounts to prevent masking and overspending. |

Benchmark reserve amounts | Target 3–6 months of operating expenses for operating reserves and 5–10% of monthly rent for capital reserves. |

Property-level tracking | Track reserve balances per property, not just portfolio-wide, to catch individual asset shortages early. |

Automate contributions | Set monthly automatic transfers to reserve accounts on rent collection day to maintain discipline. |

Annual review required | Adjust reserve contributions every year based on property age, completed projects, and current market costs. |

The mistake i see most often with reserve funds

Most landlords I work with are not reckless. They are just optimistic. They look at a $30,000 portfolio cash balance and feel secure, without realizing that one property is carrying a 15-year-old HVAC and has $800 in its reserve account.

The fix is not saving more money overall. It is tracking money at the property level. Once you assign reserves to specific addresses rather than a single pooled account, the picture changes immediately. You see which properties are well-funded and which ones are quietly building toward a crisis.

The second mistake is over-saving to the point where capital sits idle. Reserves should be sized to your actual risk, not padded indefinitely out of anxiety. A newer property with no deferred maintenance does not need a $20,000 capital reserve. That money earns more working elsewhere in your portfolio. The goal is precision, not a security blanket.

The third mistake is treating reserve contributions as optional during strong cash flow months. That is exactly when you should be building reserves, because strong cash flow will not last forever. Discipline in good months is what protects you in bad ones.

— Main

How 2ndstreetpropertymanagement helps you get this right

Managing reserve funds correctly requires systems, not just intentions. 2ndstreetpropertymanagement works with investors to build property-level financial plans that include reserve fund targets, contribution schedules, and maintenance forecasts built around each asset’s actual condition.

If you are managing a growing portfolio and want a maintenance planning system that protects your cash flow and keeps your reserves properly funded, 2ndstreetpropertymanagement has the tools and experience to build it with you. From reserve fund setup to capital expenditure forecasting, the team at 2ndstreetpropertymanagement treats your investment the way an investor would. Explore the full range of property management services and see how disciplined reserve management translates directly into better returns.

FAQ

What is a rental property reserve fund?

A rental property reserve fund is a dedicated cash account set aside to cover vacancies, unexpected repairs, and major capital expenses. It is kept separate from operating accounts to maintain financial clarity and prevent accidental overspending.

How much should i keep in a reserve fund for rentals?

Individual rental properties should maintain 3–6 months of operating expenses as an operating reserve, plus 5–10% of monthly rent directed into a capital reserve account. Older properties or those with aging systems warrant higher contributions.

What is the difference between an operating reserve and a capital reserve?

Operating reserves cover routine maintenance, minor repairs, and vacancy periods. Capital reserves fund major replacements like roofs and HVAC systems. Keeping them in separate accounts prevents one from masking shortfalls in the other.

Should reserve funds be kept in a separate bank account?

Yes. Using dedicated business bank accounts for reserve funds simplifies accounting, eases tax reporting, and adds asset protection. A high-yield savings account works well for capital reserves, while a separate checking account suits operating reserves.

How often should i review my reserve fund contributions?

Review reserve contributions at least once per year, and also after any major capital project. Adjust monthly contributions based on the property’s current age, completed repairs, and any new lender requirements.

Recommended

Comments