Rental Property Depreciation Explained for Investors

- Rey Rey Rodriguez

- 4 hours ago

- 9 min read

Rental property depreciation is a tax deduction that lets landlords recover the cost of their building over time, reducing taxable rental income without spending an extra dollar. The IRS formally calls this cost recovery, and for residential rental properties, it runs across a 27.5-year straight-line period under the Modified Accelerated Cost Recovery System (MACRS). What makes depreciation genuinely powerful is that it offsets real income even when your property is appreciating in value. You report it on Schedule E and Form 4562, and if you are not using it, you are leaving one of the most reliable tax benefits of depreciation on the table.

How is rental property depreciation calculated?

The calculation starts with your cost basis, which is the purchase price of the property minus the value of the land. Land is excluded from depreciation because it does not wear out. That distinction matters more than most investors realize, since overallocating to land shrinks your annual deduction.

Once you have your depreciable basis, the math is straightforward:

Determine the total purchase price of the property.

Subtract the assessed land value (use your county tax assessment or an appraisal to support the allocation).

Divide the remaining building value by 27.5 to get your annual depreciation deduction.

Apply the IRS mid-month convention for the first year.

Report the deduction on Form 4562 and carry it to Schedule E.

Here is a concrete example. You purchase a single-family rental for $330,000. The county assessment allocates $60,000 to land. Your depreciable basis is $270,000. Divide by 27.5 and you get $9,818 per year in depreciation.

The IRS mid-month convention treats the placed-in-service date as the midpoint of the month, which means placing a property in service in January gives you nearly a full year of depreciation, while December gives you only half a month. Timing your acquisition or rental start date can meaningfully affect your first-year deduction.

Scenario | Depreciable Basis | Annual Depreciation |

$330,000 purchase, $60,000 land | $270,000 | $9,818 |

$500,000 purchase, $100,000 land | $400,000 | $14,545 |

$200,000 purchase, $40,000 land | $160,000 | $5,818 |

Pro Tip: Get a formal land-versus-building allocation from a licensed appraiser at purchase. A defensible allocation maximizes your depreciable basis and holds up under IRS scrutiny far better than a rough estimate.

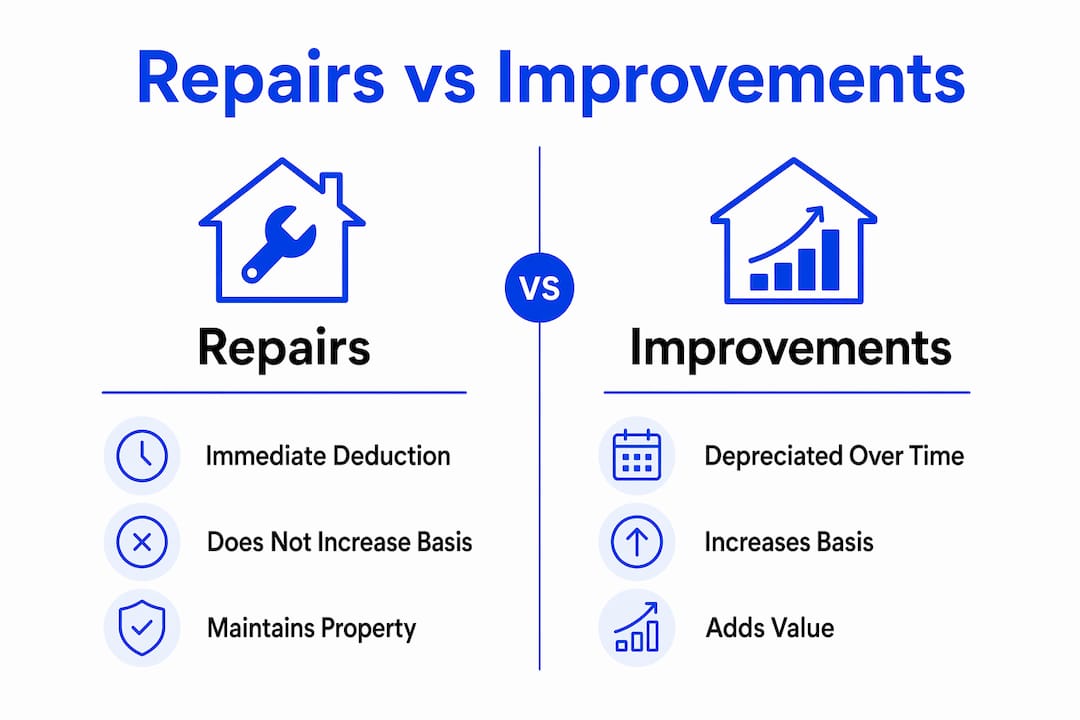

Repairs vs. improvements: what is the difference for depreciation?

This distinction trips up more landlords than almost any other tax issue. Repairs are deducted immediately in the year you pay for them, while improvements must be capitalized and depreciated over time. Getting this wrong in either direction costs you money.

The IRS uses three tests to define an improvement: betterment, restoration, or adaptation. Betterment means the work adds value or fixes a pre-existing defect. Restoration means it returns the property to working condition after deterioration. Adaptation means it changes the property’s use. If the work meets any of these criteria, it is a capital improvement, not a repair.

Practical examples make this clearer:

Replacing a broken window pane: repair, deduct now.

Replacing all windows in the building with new double-pane units: improvement, capitalize and depreciate.

Fixing a leaking pipe: repair, deduct now.

Replacing the entire plumbing system: improvement, capitalize and depreciate.

Patching a section of roof: repair, deduct now.

Full roof replacement: improvement, capitalize and depreciate.

Improvements also increase your depreciable basis, which affects both your annual deduction going forward and your gain calculation at sale. Keep every receipt, contractor invoice, and permit record. Misclassifying a capital improvement as a repair is one of the most common triggers for IRS audit adjustments on rental property returns. You can find a practical breakdown of how to budget for repairs without blurring the line into capital territory.

Pro Tip: Create a separate folder for each property year with two subfolders: “Repairs” and “Improvements.” This simple habit makes tax preparation faster and audit defense straightforward.

How does depreciation recapture work when you sell?

Depreciation recapture is the IRS mechanism that taxes back the deductions you took when you eventually sell the property. Specifically, the gain attributable to depreciation is taxed as unrecaptured §1250 gain at a maximum federal rate of 25%, separate from the capital gains rate on the rest of your profit.

Here is how the numbers work in sequence:

Calculate your adjusted basis: original purchase price plus improvements minus total depreciation taken.

Subtract the adjusted basis from the sale price to get your total gain.

Identify the portion of the gain equal to total depreciation taken. That amount is subject to the 25% recapture rate.

Any remaining gain above that is taxed at long-term capital gains rates (0%, 15%, or 20% depending on your income).

State taxes may apply separately on top of federal recapture.

The rule that catches investors off guard is the allowed or allowable standard. The IRS taxes you on depreciation you were entitled to take, whether or not you actually claimed it. If you skipped depreciation for five years, you still owe recapture tax on those five years when you sell. There is no benefit to not claiming it.

“Depreciation recapture applies to allowed or allowable depreciation even if you did not claim it, making careful tracking essential.” — Reed Corporation CPA Firm

Three planning strategies reduce or defer recapture exposure. A 1031 exchange defers all gain, including recapture, by rolling proceeds into a like-kind property. An installment sale spreads the gain and recapture tax across multiple years, smoothing the tax hit. Timing the sale in a year when your other income is lower can reduce the effective rate on the capital gain portion, though the 25% recapture rate is a ceiling, not a variable. Understanding how cash flow and taxable income diverge is the foundation for planning around recapture effectively.

What advanced strategies maximize depreciation benefits?

Standard straight-line depreciation over 27.5 years is the baseline. Sophisticated investors use cost segregation and bonus depreciation to front-load deductions and improve early-year cash flow significantly.

Cost segregation identifies components of a property that qualify for shorter recovery periods: 5, 7, or 15 years instead of 27.5. Personal property components like carpeting, appliances, and certain fixtures fall into 5-year or 7-year categories. Land improvements like parking lots and landscaping typically qualify for 15-year treatment. A cost segregation study, performed by a qualified engineer or CPA, reclassifies these components and accelerates the depreciation deductions into the early years of ownership.

Strategy | Recovery Period | Best For |

Standard MACRS depreciation | 27.5 years | All residential rentals |

Cost segregation (personal property) | 5 to 7 years | Properties with significant fixtures or equipment |

Cost segregation (land improvements) | 15 years | Properties with parking, landscaping, or fencing |

Bonus depreciation | Immediate (phasing down) | New or used property placed in service |

Bonus depreciation allows you to deduct a large percentage of qualifying property in the year it is placed in service. The rate has been phasing down from 100% and continues to step down through 2026 under current tax law. Pairing cost segregation with bonus depreciation on the reclassified components can generate substantial first-year deductions on a property that would otherwise produce modest annual write-offs. The 2025 bonus depreciation changes are worth reviewing before you place any new asset in service this year.

Section 179 expensing applies to certain personal property used in rental activity but has significant limitations for residential rental real estate. It generally cannot create a loss from rental activity, which limits its utility compared to bonus depreciation for most landlords.

Pro Tip: Commission a cost segregation study in the same year you acquire or substantially renovate a property. Retroactive studies are possible but require amended returns, which adds cost and complexity.

What IRS forms and recordkeeping practices matter most?

Proper filing and documentation are what separate investors who benefit from depreciation and those who face problems at audit or sale. The two core forms are Form 4562 and Schedule E.

Form 4562 is filed in the year you first place a property in service and in any year you add improvements or new assets. It reports the depreciation method, recovery period, and deduction amount for each asset.

Schedule E is where rental income, expenses, and the depreciation deduction from Form 4562 come together to calculate your net rental income or loss.

Beyond the forms, your recordkeeping system needs to track:

The original purchase price and the land-versus-building allocation with supporting documentation.

Every capital improvement, including the date placed in service, cost, and recovery period.

Cumulative depreciation taken each year, which becomes your depreciation schedule.

Any partial asset disposals, such as replacing a roof that was previously capitalized.

Depreciation reported on Schedule E must reconcile with Form 4562 across every year you own the property. Gaps in that record create problems when you sell and need to calculate your adjusted basis accurately. A CPA who specializes in real estate investment is worth the cost, particularly if you own multiple properties or have completed improvements that required capitalization.

Key takeaways

Rental property depreciation is a non-cash deduction that reduces taxable income annually, but it triggers recapture tax at sale, making accurate tracking and proactive planning non-negotiable for every landlord.

Point | Details |

Depreciable basis excludes land | Subtract land value from purchase price before dividing by 27.5 for your annual deduction. |

Mid-month convention affects year one | Placing property in service earlier in the year increases your first-year depreciation deduction. |

Repairs vs. improvements | Repairs are deducted immediately; improvements are capitalized and depreciated over time. |

Recapture applies regardless of claims | The IRS taxes allowed or allowable depreciation at sale, even if you never claimed the deduction. |

Cost segregation accelerates deductions | Reclassifying components to 5, 7, or 15-year periods front-loads deductions and improves cash flow. |

Why most landlords underuse their single best tax tool

I have reviewed the financials of enough rental portfolios to say this with confidence: depreciation is the most underused legal tax tool available to landlords, and the reason is almost always a misunderstanding of what it actually does. Investors see their property value rising and assume depreciation is some kind of accounting fiction. It is not. Depreciation allows deductions even when property value increases, which means you are reducing your tax bill in years when your net worth is growing. That combination is rare in any asset class.

The mistake I see most often is treating every contractor invoice as a repair. Replacing a water heater for $1,200 is a repair. Gutting and rebuilding a kitchen for $40,000 is a capital improvement. Blurring that line does not save you money. It either accelerates a deduction you should have spread out or delays one you could have taken immediately, and it creates audit exposure either way.

The recapture issue deserves more attention than most investors give it. I have spoken with landlords who deliberately skipped depreciation because they wanted to avoid recapture at sale. That logic is backwards. The IRS taxes you on what you were allowed to claim, not just what you claimed. Skipping the deduction costs you real money now and saves you nothing later.

If you own a property worth more than $500,000 or have recently completed a major renovation, a cost segregation study is worth a serious conversation with your CPA. The upfront cost of the study is typically recovered in the first year through accelerated deductions. Done early with solid documentation, it is one of the highest-return decisions you can make in your first year of ownership.

— Main

How 2ndstreetpropertymanagement helps you maximize your investment

At 2ndstreetpropertymanagement, we are investors ourselves, which means we understand that tax efficiency is not a side benefit of rental property ownership. It is a core part of your return.

Our team supports landlords with financial reporting, expense documentation, and the organized records that make depreciation tracking and tax preparation straightforward. Whether you are managing your first rental or scaling a portfolio, having clean, accurate records from day one protects your basis calculations and keeps your CPA focused on strategy rather than reconstruction. Visit 2ndstreetpropertymanagement.com to learn how we help investors maximize rental property income while keeping the financial side of ownership under control.

FAQ

What is rental property depreciation?

Rental property depreciation is a tax deduction that lets landlords recover the cost of the building portion of a rental property over 27.5 years using the IRS straight-line method under MACRS. It reduces taxable rental income each year without requiring any additional cash outlay.

Can I depreciate land on a rental property?

No. Land does not depreciate and is excluded from the depreciable basis. You must subtract the land value from the total purchase price before calculating your annual depreciation deduction.

What happens to depreciation when I sell a rental property?

The IRS taxes the portion of your gain equal to total depreciation taken as unrecaptured §1250 gain at a maximum federal rate of 25%. This applies to all depreciation you were allowed to claim, even if you did not actually take the deductions.

What is cost segregation and who should use it?

Cost segregation is a study that reclassifies building components into shorter depreciation periods (5, 7, or 15 years) to accelerate deductions. It is most valuable for investors who acquire or renovate properties with a cost basis above $300,000 and want to maximize early-year tax savings.

Do I have to file Form 4562 every year for my rental property?

You file Form 4562 in the year you first place the property in service and in any year you add new depreciable assets or improvements. In other years, depreciation from prior Form 4562 filings carries forward automatically to Schedule E.

Recommended

Comments