How to Analyze a Rental Property Deal Like a Pro

- Rey Rey Rodriguez

- 3 days ago

- 8 min read

Analyzing a rental property deal is the process of calculating key financial metrics to determine whether a property will generate acceptable returns relative to its purchase price and financing costs. Most investors who lose money on rentals don’t lose it at closing. They lose it during underwriting, when optimistic assumptions replace disciplined math. Tools like DealCheck, BiggerPockets calculators, and the NOI framework exist precisely to prevent that. This guide walks you through every step of rental property investment analysis, from income estimation through stress testing, so you make offers based on numbers, not hope.

What key metrics should you calculate when analyzing a rental property deal?

Every metric in a rental property evaluation tells a different part of the same story. Relying on just one is like comparing two vehicles using only horsepower. You need the full picture before you can make a sound decision.

Here are the core property investment metrics every investor must calculate:

Net Operating Income (NOI): Gross rental income minus all operating expenses, excluding debt service. NOI isolates the property’s operational performance from your financing structure, which makes it the foundation for every other metric. NOI before financing is the number that tells you how the asset performs on its own terms.

Capitalization Rate (Cap Rate): NOI divided by the purchase price. Cap rate measures unleveraged yield and lets you compare properties across markets without the noise of different loan structures. A detailed breakdown of cap rate calculation shows why this metric is indispensable for market comparisons.

Cash Flow: NOI minus your annual debt service. This is your actual take-home profit after the mortgage is paid. Positive cash flow is the goal; negative cash flow means the property costs you money every month.

Cash-on-Cash Return: Annual cash flow divided by total cash invested (down payment plus closing costs plus any upfront repairs). This reflects your leveraged return on the actual dollars you put in, not the full purchase price.

Debt Service Coverage Ratio (DSCR): NOI divided by annual debt service. A DSCR below 1.0 means the property cannot cover its own debt payments. A DSCR above 1.25 signals comfortable coverage and is typically what lenders require for loan approval.

Pro Tip: Before running any full analysis, apply the rent-to-price ratio as a quick filter. Properties with a rent-to-price ratio at or above 0.7% are worth deeper analysis. Anything below 0.5% is almost always a cash flow problem waiting to happen.

One additional quick screen worth knowing: the 1% rule states that monthly rent should equal at least 1% of the purchase price. It’s a rough heuristic, not a final verdict, but it filters out obvious underperformers in seconds.

How to estimate realistic rental income and operating expenses

Accurate underwriting starts with honest numbers, not the best-case scenario the seller’s broker presents. Verifying rental income from actual rent rolls and comparable listings, and verifying expenses from utility bills and tax records, is the foundation of credible analysis.

For rental income, pull at least three to five comparable active listings in the same submarket. Cross-reference those with recently leased units, not just asking rents. Then apply a vacancy rate of 5% to 8% to account for turnover, lease-up periods, and unexpected vacancies. Skipping this step is one of the most common and costly mistakes new investors make.

Operating expenses to itemize include:

Property taxes: Pull the actual tax bill, not an estimate.

Insurance: Get a real quote for landlord or dwelling fire coverage.

Property management fees: Typically 8% to 12% of collected rent, even if you self-manage. Model it in anyway, because your time has value and circumstances change.

Maintenance and repairs: Budget 1% of property value annually as a baseline for older properties, and adjust upward for deferred maintenance.

Capital expenditure reserves: Set aside funds for roof, HVAC, water heater, and appliance replacements. A common reserve target is $100 to $150 per unit per month.

Utilities paid by owner: Trash, water, and sewer if the lease structure requires it.

Pro Tip: Use two independent layers of comps when evaluating a deal. One set validates the purchase price against recent sales. A separate set validates the projected rental income against current leases. Conflating the two creates blind spots that distort every downstream metric.

The most common underwriting errors are overestimating rent by 10% to 15% above market, ignoring vacancy entirely, and treating deferred maintenance as a cosmetic issue rather than a capital cost. Conservative estimates protect your cash flow projections when reality diverges from the spreadsheet.

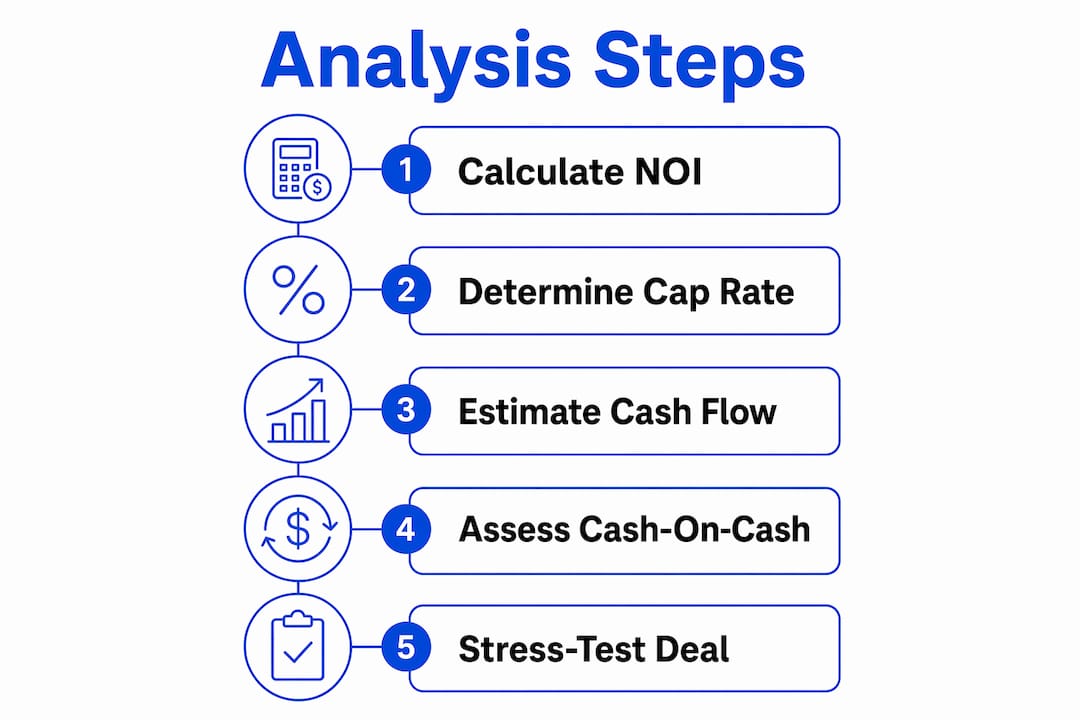

Step-by-step financial calculation process for a rental property

A comprehensive underwriting process follows a clear sequence: estimate income, subtract expenses to get NOI, compute cap rate, model the mortgage, calculate cash flow, determine cash-on-cash return, and evaluate DSCR. Here is that sequence applied to a concrete example.

Assume a property listed at $250,000 with projected gross rents of $2,400 per month.

Calculate Effective Gross Income (EGI): Multiply monthly rent by 12, then subtract vacancy. At 7% vacancy: $28,800 x 0.93 = $26,784 annually.

Subtract operating expenses: If total annual operating expenses are $10,000 (taxes, insurance, management, maintenance, reserves), your NOI is $26,784 minus $10,000 = $16,784.

Compute cap rate: $16,784 divided by $250,000 = 6.7%. This is your unleveraged yield.

Model the mortgage payment: On a $200,000 loan (20% down) at 7% interest over 30 years, annual debt service is approximately $15,984.

Calculate cash flow: $16,784 NOI minus $15,984 debt service = $800 annual cash flow, or about $67 per month.

Determine cash-on-cash return: Total cash invested is $50,000 down plus $5,000 in closing costs = $55,000. Cash-on-cash return is $800 divided by $55,000 = 1.5%. That’s thin. Most investors target 6% to 10%.

Evaluate DSCR: $16,784 divided by $15,984 = 1.05. This clears the 1.0 threshold but falls short of the 1.25 lenders prefer.

Metric | Value | Benchmark |

NOI | $16,784 | Higher is better |

Cap Rate | 6.7% | Market dependent |

Annual Cash Flow | $800 | Positive required |

Cash-on-Cash Return | 1.5% | Target 6%+ |

DSCR | 1.05 | Lenders prefer 1.25+ |

Now stress-test the deal. Reduce projected rents by 15% to 20% and increase vacancy to 10%. If the deal still produces positive cash flow under those conditions, you have a durable investment. If it goes negative, you know the deal only works under ideal conditions, which is a risk most disciplined investors avoid.

Pro Tip: If the deal doesn’t work at the asking price, reverse-engineer it. Calculate the maximum purchase price that produces your target cash-on-cash return under stress-tested assumptions. That number becomes your ceiling offer, not a starting point for negotiation.

What common mistakes should you avoid when analyzing rental deals?

The errors that sink rental investments are almost always made during underwriting, not during ownership. Recognizing them before you make an offer is the difference between a performing asset and a money pit.

Including mortgage payments in NOI: Mixing debt payments into NOI is a common beginner mistake that distorts every metric downstream. NOI is pre-financing by definition. Keep debt service separate.

Ignoring vacancy: Assuming 100% occupancy is not conservative underwriting. It’s wishful thinking. Apply a realistic vacancy rate of at least 5% to 8% in stable markets, and higher in transitional ones.

Skipping DSCR before assuming financing: Small variations in PITIA calculations can determine whether a lender approves your loan. Run DSCR before you assume the financing works.

Overvaluing rental income without comps: Accepting the seller’s projected rents without independent verification is a due diligence failure. Always validate with current market data.

Not stress-testing assumptions: Deals that only work under best-case conditions are not deals. They are bets. Conservative stress-testing separates durable investments from fragile ones.

Neglecting physical due diligence: Deferred maintenance on roofs, HVAC systems, and plumbing translates directly into capital expenditures that destroy your first two to three years of cash flow. Always inspect before you underwrite final numbers.

Pro Tip: Use a quick deal framework to screen deals in under 15 minutes before committing to full underwriting. It saves hours and filters out obvious losers early.

Key takeaways

Disciplined rental property analysis requires calculating NOI, cap rate, cash flow, cash-on-cash return, and DSCR in sequence, then stress-testing every assumption before making an offer.

Point | Details |

NOI is the foundation | Calculate NOI before financing to isolate true operational performance from loan structure. |

DSCR determines loan viability | A DSCR above 1.25 signals lender-acceptable coverage; below 1.0 means the property can’t cover its debt. |

Stress-test every deal | Reduce rents 15% to 20% and raise vacancy to confirm the deal survives realistic downside scenarios. |

Verify income and expenses independently | Use rent rolls, comps, and actual bills rather than seller projections to build credible underwriting. |

Reverse-engineer your offer price | If the deal fails at asking price, calculate the maximum price that meets your return threshold and offer that. |

Why I think most investors analyze deals backward

Most investors I’ve seen start with the asking price and work forward to see if the numbers “work.” That’s the wrong direction. It confuses movement with progress. You end up rationalizing a price rather than evaluating a deal.

The right approach starts with your required return. What cash-on-cash return do you need to justify the risk and capital? Work backward from that number to find the maximum price you can pay. If the seller won’t meet that price, you walk. That discipline is what separates investors who build portfolios from those who own one property that barely breaks even.

Financing structure also matters far more than most first-time investors realize. Two investors buying the same property at the same price can produce dramatically different returns based purely on loan terms, rate locks, and down payment size. Model multiple financing scenarios before you commit to one.

The emotional pull of a “great neighborhood” or a “beautiful renovation” is real, and it kills returns. The numbers don’t care about curb appeal. Run the analysis cold, share it with a peer who will push back, and only then let your conviction grow. The deals that survive scrutiny are the ones worth owning.

— Main

How 2ndstreetpropertymanagement helps you evaluate and manage rental investments

2ndstreetpropertymanagement is built by investors, for investors. The team understands that a great property management relationship starts before you close, not after. Whether you need help validating rental income assumptions, understanding local vacancy rates, or modeling management fees into your underwriting, 2ndstreetpropertymanagement brings real market data to the table. Explore property management services designed to protect your cash flow, reduce vacancy, and give you the operational support that turns a good deal on paper into a performing asset in practice.

FAQ

What is the most important metric when evaluating a rental property?

NOI is the foundational metric because it measures a property’s operational performance independent of financing. Every other metric, including cap rate, cash flow, and DSCR, is derived from it.

What DSCR do lenders typically require for rental property loans?

Most lenders require a DSCR above 1.25 for rental property financing. A DSCR below 1.0 means the property cannot cover its own debt payments, which disqualifies it from most loan programs.

How do you stress-test a rental property deal?

Reduce your projected rents by 15% to 20% and increase your assumed vacancy rate, then recalculate cash flow and DSCR under those conditions. If the deal still produces positive returns, the investment is built on durable assumptions.

What is a good cash-on-cash return for a rental property?

Most experienced investors target a cash-on-cash return of 6% to 10% on stabilized rental properties. Returns below 5% often indicate thin margins that leave little room for unexpected expenses or market softening.

How do you calculate cap rate for a rental property?

Cap rate equals NOI divided by the purchase price. A $15,000 NOI on a $200,000 property produces a 7.5% cap rate. This metric lets you compare properties across different markets and financing structures on equal terms.

Recommended

Comments