Rental Property Bookkeeping Explained for Landlords

- Rey Rey Rodriguez

- 2 days ago

- 8 min read

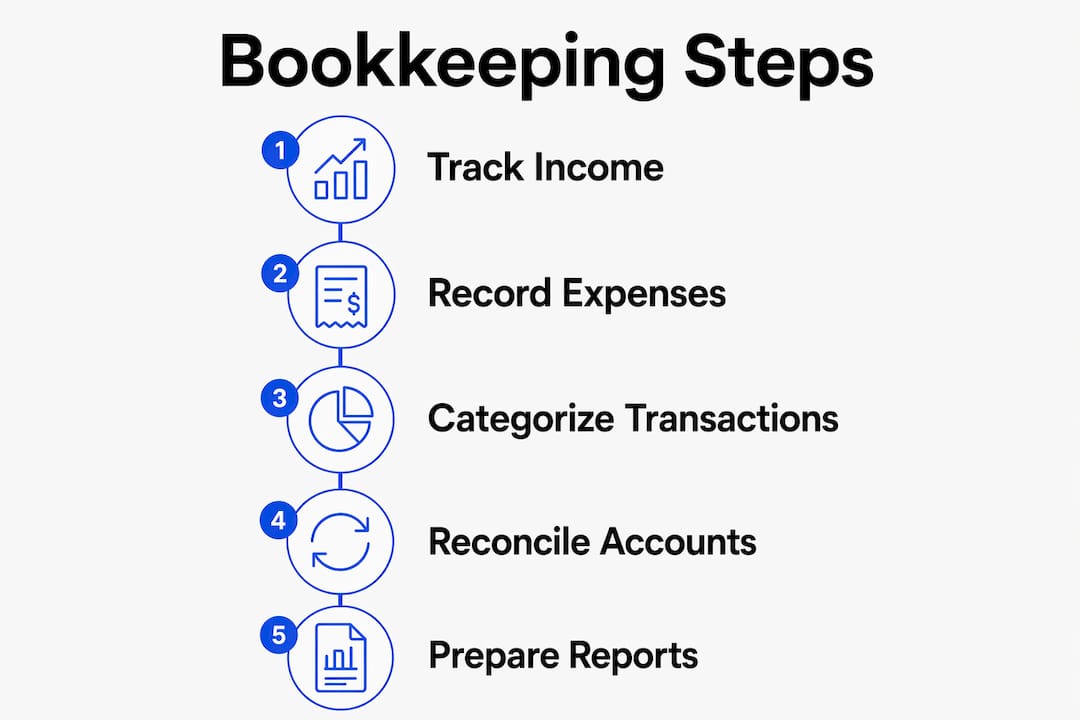

Rental property bookkeeping is the systematic process of recording, categorizing, and reporting every dollar of income and expense tied to your rental real estate. Done correctly, it keeps you IRS-compliant, maximizes your deductions, and gives you the financial clarity to make smart investment decisions. Tools like QuickBooks Online, TurboTenant, and VerticalRent have made this process far more accessible, but the foundation is always the same: clean records aligned with IRS Schedule E reporting requirements. Whether you own one rental or ten, understanding rental property bookkeeping explained from the ground up is the difference between a profitable portfolio and a tax-time disaster.

What is rental property bookkeeping and why does it matter?

Rental property bookkeeping, known in accounting circles as real estate bookkeeping or property management accounting, is the practice of maintaining organized financial records for each rental unit you own. The IRS requires you to report rental income and expenses on Form 1040 Schedule E, listing total income, deductible expenses, and depreciation for each property. That requirement alone defines the structure your books must follow.

The stakes are real. Misreporting rental income or claiming unsupported deductions can trigger an accuracy-related penalty of up to 20% of the underpayment. That is not a rounding error. It is a direct cost of poor recordkeeping that every landlord can avoid with the right system in place.

Beyond tax compliance, clean books tell you whether a property is actually performing or just consuming your attention. Cash flow, net operating income, and return on investment are only meaningful numbers when the underlying data is accurate. Bookkeeping is not just an accounting task. It is the foundation of every sound investment decision you make.

How to set up a chart of accounts for rental properties

A chart of accounts divides all your transactions into assets, liabilities, revenue, and expenses, and it should mirror the line items on Schedule E. This alignment is what makes tax preparation fast and audit defense straightforward. Without it, you are doing double work every April.

Income categories to track

Your revenue accounts should separate income types rather than lumping everything into a single “rent received” bucket. Typical income accounts include:

Rental income: Base rent payments from tenants

Late fees: Charged when rent is paid past the due date

Pet fees and pet rent: Monthly or one-time charges for animals

Parking and storage fees: Separate from base rent

Reimbursed expenses: Utility pass-throughs or repair reimbursements

Separating residential from commercial rent income matters because tax treatment differs between the two, and Schedule E reporting requirements are not identical. Keeping these accounts distinct saves your CPA hours of untangling at year-end.

One account that trips up many landlords: security deposits. These are not income when collected. They are a liability until you apply them to unpaid rent or damages. Tenant-held funds must stay separate from earned income to avoid misclassification and potential regulatory issues.

Expense categories aligned with Schedule E

Schedule E Line | Expense Category | Examples |

Line 5 | Advertising | Listing fees, signage, photography |

Line 6 | Auto and travel | Mileage to inspect properties |

Line 9 | Insurance | Landlord policy, umbrella coverage |

Line 11 | Legal and professional | CPA fees, attorney costs |

Line 13 | Management fees | Property management charges |

Line 14 | Mortgage interest | Paid to banks and lenders |

Line 16 | Repairs | Maintenance, plumbing, HVAC service |

Line 18 | Depreciation | Calculated via Form 4562 |

Depreciation deserves special attention. The IRS requires you to use Form 4562 to calculate depreciation entered on Schedule E line 18. Residential rental property depreciates over 27.5 years under the Modified Accelerated Cost Recovery System. Missing this deduction is one of the most expensive mistakes a landlord can make.

Pro Tip: Classify capital improvements separately from repairs. A new roof is a capital improvement depreciated over time. Patching a leak is a repair deducted in full the year it occurs. Mixing these up costs you deductions and creates audit exposure.

How to track rental income and expenses accurately

Accurate rental income tracking starts before the money hits your account. Every payment you receive, including advance rents, partial payments, late fees, and utility reimbursements, counts as taxable income in the year you receive it under cash basis accounting. The IRS does not care that a tenant paid January rent in December. You received it in December, so it belongs in that tax year.

Follow these steps to build an audit-ready recordkeeping system:

Open a dedicated bank account for each property or portfolio. Mixing personal and rental funds is the single fastest way to create tax errors and invite IRS scrutiny. A separate account makes reconciliation clean and defensible.

Collect and file documentary evidence for every expense. The IRS mandates receipts or canceled checks to substantiate deductible expenses. A verbal agreement with a contractor is not documentation. A paid invoice is.

Log transactions weekly, not monthly. Weekly transaction capture prevents what accountants call “mystery expenses,” those charges you cannot explain six months later. It also supports the thorough documentation IRS audit standards require.

Reconcile your bank accounts monthly. Compare your accounting software records against your bank statement line by line. Discrepancies caught monthly take minutes to resolve. Discrepancies caught in March for the prior year take hours.

Track mileage separately. Every trip to inspect a property, meet a contractor, or show a unit is potentially deductible. Apps like MileIQ or the mileage log in QuickBooks Self-Employed make this automatic.

Pro Tip: Use your rental property checklist to cross-reference your bookkeeping records at lease start and end. Move-in and move-out documentation directly supports your security deposit accounting and any damage deductions.

How does per-property financial tracking work for multiple rentals?

Property management accounting requires tracking financial transactions at multiple levels: tenant, unit, property, and owner. When you own more than one rental, this multi-dimensional tracking is not optional. It is the only way to know which properties are performing and which are quietly draining your returns.

QuickBooks Online handles this through its Class or Location tracking feature. You assign each property as a separate class or location, and every transaction gets tagged accordingly. The result is a per-property profit and loss statement you can generate in minutes. That report is what your CPA needs to complete Schedule E, what a lender needs to evaluate a refinance, and what you need to decide whether to hold or sell a property.

Schedule E supports up to three properties per form. If you own more, the IRS requires continuation pages. This is a structural reason why per-property reporting matters from day one. Trying to untangle commingled records across four or five properties at tax time is the kind of problem that costs you both money and sleep.

Generate a per-property profit and loss statement monthly, not just at year-end

Use subaccounts or tags to separate income and expenses by unit within a multi-unit property

Keep a separate depreciation schedule for each property, updated annually

Store all property-specific documents (purchase closing statements, improvement receipts, insurance policies) in a dedicated digital folder per property

Pro Tip: Tools like property maintenance tracking software can integrate with your accounting system to automatically log repair expenses by property and unit, eliminating manual data entry for one of your most frequent expense categories.

Best practices to avoid costly bookkeeping mistakes

The most common landlord bookkeeping failures are not complex accounting errors. They are discipline failures: skipping weekly updates, using one bank account for everything, and guessing at expense categories instead of verifying them.

Commingling personal and rental funds is the most damaging habit. It does not just create tax confusion. It can trigger IRS penalties and, in the case of an LLC-owned property, potentially pierce the corporate veil that protects your personal assets. Open a dedicated checking account for each property or at minimum for your entire rental portfolio, and never run a personal expense through it.

Misclassifying repairs versus capital improvements is the second most expensive mistake. Replacing a broken window is a repair. Replacing all windows in the building as part of a renovation is a capital improvement. The distinction determines whether you deduct the full cost this year or depreciate it over years. When you are budgeting for rental property repairs, document the scope of work clearly so the classification is defensible.

Automated expense categorization tools that tag transactions directly to Schedule E categories and log them by property can dramatically reduce the time you spend on bookkeeping. VerticalRent’s AI-based system, for example, auto-logs expenses per property and unit with IRS-aligned categorization. The technology does not replace judgment, but it eliminates the manual tagging that most landlords find most tedious.

Pro Tip: Design your chart of accounts and tagging system from the start to produce Schedule E-ready financials without year-end retroactive categorization. Retroactive cleanup is always slower and more error-prone than real-time entry.

Key takeaways

Rental property bookkeeping done right means your books are always audit-ready, your Schedule E is accurate, and your per-property financials tell you exactly where your money is going.

Point | Details |

Align accounts with Schedule E | Build your chart of accounts to mirror Schedule E line items from day one to simplify tax filing. |

Separate funds by property | Use dedicated bank accounts to prevent commingling and protect against IRS penalties. |

Document every deduction | Keep receipts, invoices, and canceled checks for all expenses; the IRS requires documentary evidence. |

Track depreciation separately | Use Form 4562 annually and maintain a per-property depreciation schedule to capture this critical deduction. |

Update books weekly | Weekly transaction entry prevents mystery expenses and keeps your records audit-ready year-round. |

Why most landlords overcomplicate this (and what actually works)

After working with rental property investors across multiple markets, one pattern stands out: landlords who struggle with bookkeeping are almost never struggling with accounting concepts. They are struggling with consistency. They know what a chart of accounts is. They just have not built the habit of updating it every week.

The investors who get this right treat their books the way they treat rent collection. It is a non-negotiable weekly task, not a quarterly scramble. They use software like QuickBooks Online or TurboTenant to automate what can be automated, and they spend 20 to 30 minutes a week reviewing what cannot. That discipline compounds over time. By the time tax season arrives, their CPA has clean, per-property financials and the filing takes hours, not days.

The myth I hear most often is that spreadsheets are “good enough” for small portfolios. They are not. A spreadsheet cannot reconcile against your bank account automatically. It cannot generate a per-property profit and loss statement in one click. It cannot flag a transaction that was miscategorized six months ago. The moment you own more than two properties, a spreadsheet becomes a liability, not an asset.

The other misconception worth addressing: bookkeeping is not just a tax exercise. Your books are a decision-making tool. When you are evaluating whether to refinance, sell, or acquire another property, clean per-property financials are what separate a data-driven decision from a gut feeling. Investors who treat bookkeeping as a tax chore miss the strategic value sitting inside their own records.

— Main

Let 2ndstreetpropertymanagement handle the financial complexity

Managing rental property finances takes more than good intentions. It takes systems, discipline, and expertise that most landlords build slowly through expensive trial and error.

At 2ndstreetpropertymanagement, we built our financial management services specifically for rental property investors who want clean books, audit-ready records, and per-property reporting without spending their weekends on accounting software. Our team understands Schedule E compliance, expense categorization, and the reporting standards lenders and CPAs actually need. If you are ready to stop guessing and start managing your rental finances with the same rigor you apply to your investments, we are built for that conversation.

FAQ

What is rental property bookkeeping?

Rental property bookkeeping is the process of recording and categorizing all income and expenses related to your rental properties. It produces the financial records needed for IRS Schedule E reporting, tax compliance, and investment analysis.

What expenses can landlords deduct on Schedule E?

Landlords can deduct advertising, insurance, mortgage interest, repairs, management fees, legal fees, and depreciation, among other expenses. The IRS requires documentary evidence such as receipts or canceled checks to support every deduction claimed.

Do I need separate bank accounts for each rental property?

A dedicated bank account for your rental portfolio is the minimum requirement. Mixing personal and rental funds risks IRS penalties and makes accurate per-property reporting nearly impossible.

How does depreciation work for rental property?

Residential rental property depreciates over 27.5 years using the Modified Accelerated Cost Recovery System. You calculate and report depreciation on Form 4562, and the result flows to Schedule E line 18 as a deductible expense each year.

What is the best bookkeeping software for landlords?

QuickBooks Online, TurboTenant, and VerticalRent are three widely used options for landlord accounting. QuickBooks offers the most flexibility for per-property class tracking, while TurboTenant and VerticalRent provide landlord-specific features like rent collection integration and automated Schedule E categorization.

Recommended

Comments