Rental Property Expense Tracking Best Practices

- Rey Rey Rodriguez

- 1 day ago

- 9 min read

Rental property expense tracking is the systematic process of recording, categorizing, and reconciling every cost tied to your investment properties so you capture every legal deduction and defend every number at audit. The IRS requires landlords to substantiate all expenses with receipts and records, and the gap between landlords who do this well and those who do it poorly shows up directly on Schedule E. Tools like QuickBooks Online, RentRedi, and dedicated bookkeeping workflows give you the structure to track rental expenses accurately, protect your cash flow, and make smarter portfolio decisions.

1. Rental property expense tracking best practices start with separate bank accounts

The single most impactful change most landlords can make is opening a dedicated checking account for each rental property or LLC. Mixing personal and rental funds in one account does not just create bookkeeping headaches. It destroys your audit defense and forces you to reconstruct transactions from memory at the worst possible time.

RentalReportLab recommends dedicated bank accounts per property alongside reserve funds sized at three to six months of operating expenses. That reserve discipline matters because it prevents you from dipping into operating funds for capital repairs, which distorts your true property-level profitability.

Here is what a clean account structure looks like in practice:

One operating checking account per property (or per LLC if you hold multiple properties under one entity)

A separate savings account for reserves and security deposits

A dedicated credit card used exclusively for property expenses, paid from the operating account

Pro Tip: Set up automatic transfers from rent deposits into your reserve account on the first of each month. This keeps your operating balance accurate and your reserve funded without manual effort.

RentRedi users who connect their bank accounts directly to the platform see transaction data populate automatically, which removes the manual entry step that causes most categorization errors. Per-property account separation is the foundation every other best practice builds on.

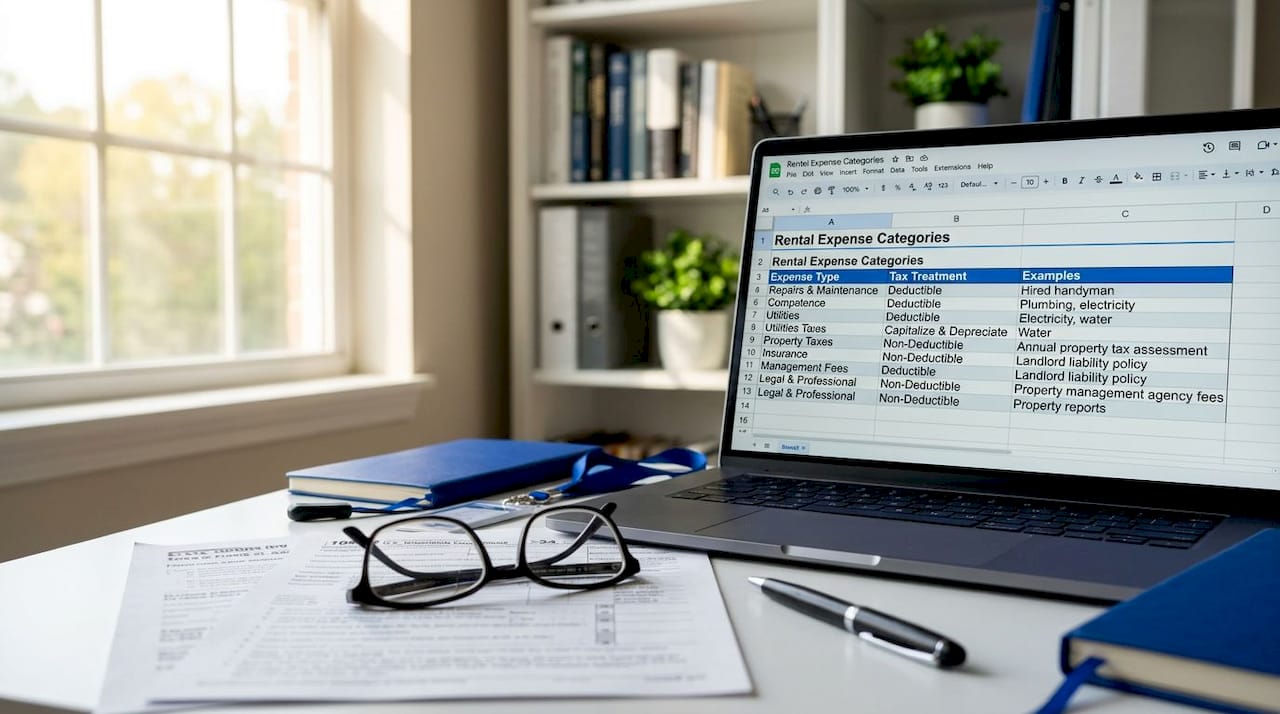

2. How to categorize rental property expenses effectively

Expense categorization aligned with IRS Schedule E is the standard industry approach to landlord bookkeeping. Schedule E organizes rental income and expenses into specific lines: advertising, auto and travel, cleaning and maintenance, commissions, insurance, legal and professional fees, management fees, mortgage interest, repairs, supplies, taxes, utilities, and depreciation. Mapping your chart of accounts to these lines from day one eliminates the year-end reclassification work that costs landlords hours and often leads to missed deductions.

The most consequential categorization decision you will make is separating repairs from capital improvements. The IRS governs this distinction under Regulation 1.263(a)-3, and misclassifying a capital improvement as a repair gives you a current deduction you are not entitled to, while misclassifying a repair as a capital improvement costs you a deduction you could have taken immediately.

Expense type | Tax treatment | Example |

Repair | Fully deductible in current year | Replacing a broken window pane |

Capital improvement | Depreciated over useful life | Installing a new HVAC system |

Maintenance | Fully deductible in current year | Annual furnace inspection |

Capital addition | Depreciated over useful life | Adding a new deck or room |

RentalReportLab advises categorizing expenses at the time of the transaction rather than batching them weekly or monthly. The logic is simple: you remember the context of a $400 plumber visit the day it happens. Three months later, you are guessing whether it was a repair or a capital improvement.

Pro Tip: Create a one-page reference sheet listing your most common vendors and the Schedule E category each one maps to. Tape it inside your bookkeeping folder or pin it in your accounting software. This alone cuts categorization time in half.

For maintenance cost details by property type, the maintenance cost categories guide from 2ndstreetpropertymanagement breaks down what belongs where with real examples.

3. Best software for expense tracking: spreadsheets vs. dedicated tools

Spreadsheets work for a single property with low transaction volume. They break down the moment you add a second property, a contractor relationship, or a CPA who needs clean reports. The real cost of a spreadsheet is not the time you spend entering data. It is the categorization errors and missing receipts you do not catch until tax season.

QuickBooks Online’s Class and Location tracking features are the gold standard for per-property profit and loss reporting. You assign each transaction a Class (property address) and a Location (portfolio or entity), which lets you pull a clean P&L for any single property in seconds. This is the level of visibility you need to make hold, sell, or refinance decisions with confidence.

Key features to look for in any expense tracking tool:

Automatic bank feed integration that pulls transactions daily

Receipt digitization via mobile photo capture

Per-property tagging or class tracking

IRS Schedule E report generation

Cloud backup with role-based access for your CPA

Bank rules in QuickBooks Online can automate 60 to 70 percent of transaction categorization once you set them up correctly. That means the majority of your monthly bookkeeping runs on autopilot, and you review exceptions rather than entering every line manually.

RentRedi combines rent collection, maintenance tracking, and expense logging in one platform, which makes it a strong choice for landlords who want property management and bookkeeping in the same workflow. For landlords who want to analyze a rental property’s financials before making decisions, pairing your tracking software with a deal analysis tool gives you both historical data and forward-looking projections.

Pro Tip: Photograph every receipt immediately using your phone. Paper receipts fade within months, and digital copies are accepted by the IRS. Store them in a folder organized by property and month so retrieval during an audit takes minutes, not hours.

4. Why separate accounts and per-property tagging protect your ROI

Tracking investment property costs at the property level is not just a bookkeeping preference. It is the only way to know whether each property in your portfolio is actually earning what you think it is. A landlord managing three properties from one bank account and one QuickBooks file is measuring portfolio averages, not property performance. That confusion costs real money when one underperforming property masks the returns of two strong ones.

Using QuickBooks Online’s Class feature or RentRedi’s per-property ledger means every income and expense transaction carries a property tag. Pull a report for Property A and you see its true net operating income, its repair-to-rent ratio, and its year-over-year expense trend. That data tells you whether to raise rents, defer maintenance, or sell. Without it, you are making portfolio decisions on instinct.

The protect cash flow guide from 2ndstreetpropertymanagement covers how property-level financial visibility directly affects your ability to defend and grow rental income over time.

5. Why regular reconciliation and review routines are critical

Monthly reconciliation is the minimum frequency recommended by accounting professionals who work with real estate investors. Catalyst CPA warns that quarterly reconciliation is the minimum acceptable standard, and annual-only reconciliation commonly results in losing 8 to 15 percent of legitimate deductions. That is not a rounding error. On a $50,000 expense year, that is $4,000 to $7,500 in deductions gone because transactions were never matched or categorized.

A practical monthly reconciliation workflow looks like this:

Download your bank statement on the last day of the month

Match every transaction in your accounting software to the bank feed

Confirm every expense has a property tag and a Schedule E category

Review any uncategorized or flagged transactions and resolve them

Run a per-property P&L and compare it to your prior month budget

“Treat reconciliation timing as a tax-risk control, not a bookkeeping chore. Every month you skip is a month of deductions you may never recover.” — Catalyst CPA

RentRedi recommends monthly reviews as the baseline, with some landlords running weekly spot checks and quarterly deeper dives into depreciation schedules and capital improvement tracking. The weekly habit is particularly useful during active renovation periods when contractor invoices arrive in batches.

Mileage and travel expenses deserve their own tracking discipline. The IRS requires contemporaneous records for vehicle use, meaning a mileage log maintained at the time of each trip. Apps like MileIQ or the built-in mileage tracker in QuickBooks Self-Employed handle this automatically.

6. Common mistakes landlords make in expense tracking

The most expensive bookkeeping mistakes are not dramatic errors. They are small, repeated failures that compound over time into significant lost deductions and audit exposure.

Commingling funds: Running personal and rental transactions through the same account makes it nearly impossible to prove which expenses were business-related during an audit.

Missing per-property tags: Entering an expense without assigning it to a specific property destroys your ability to measure individual property performance and creates reclassification work at year-end.

Confusing repairs and capital improvements: As noted under IRS Regulation 1.263(a)-3, this misclassification either accelerates deductions you are not entitled to or delays deductions you could take now.

Skipping bank reconciliations: Missing timely reconciliations is the major bookkeeping failure mode that causes lost deductions year after year.

Misclassifying security deposits: Security deposits are liabilities, not income, until you apply them. Recording them as income overstates your taxable revenue.

Ignoring IRS Publication 463: Travel expenses for property visits, inspections, and tenant meetings are deductible, but only with documentation that meets IRS standards.

Pro Tip: Set a calendar reminder for the 5th of each month labeled “Property Books.” Thirty minutes of focused reconciliation on that date prevents the four-hour scramble in April that every landlord dreads.

For a broader view of the financial mistakes that hurt rental investors most, the top costly mistakes guide from 2ndstreetpropertymanagement covers the patterns that show up repeatedly across portfolios.

Key takeaways

Disciplined rental property expense tracking, built on separate accounts, IRS-aligned categories, and monthly reconciliation, is the most direct path to maximizing deductions and protecting portfolio profitability.

Point | Details |

Separate accounts first | Open a dedicated checking account per property to simplify reconciliation and audit defense. |

Align categories to Schedule E | Map every expense to an IRS Schedule E line at the time of the transaction to avoid year-end reclassification. |

Use software with per-property tracking | QuickBooks Online Classes or RentRedi tags give you property-level P&L visibility for real investment decisions. |

Reconcile monthly without exception | Monthly reconciliation prevents losing 8 to 15 percent of legitimate deductions from untracked transactions. |

Digitize receipts immediately | Photograph receipts at the point of purchase and store them by property and month for fast audit retrieval. |

What I’ve learned from watching landlords track expenses the hard way

Most landlords I work with do not have a knowledge problem. They know they should track expenses carefully. They have a discipline problem, and specifically a systems problem. When the system requires manual effort at the end of a busy month, it does not get done.

The landlords who get this right are not necessarily more organized people. They have built workflows that make the right behavior the easy behavior. A dedicated bank account means the bank feed is already clean. Bank rules in QuickBooks mean 60 to 70 percent of transactions categorize themselves. A phone habit of photographing receipts immediately means the shoebox never fills up.

I have also seen the cost of skipping these steps. A landlord with four properties who reconciled annually lost over $6,000 in deductions in a single tax year because contractor payments were never matched to invoices and two capital improvements were never depreciated correctly. That is not a tax strategy failure. That is a recordkeeping failure with a tax consequence.

The choice between DIY bookkeeping and hiring a CPA or bookkeeper comes down to portfolio size and your honest assessment of your own consistency. One or two properties with clean bank feeds and monthly reconciliation is manageable solo. Three or more properties, active renovations, or multiple LLCs is where professional help pays for itself in deductions recovered and audit risk reduced.

— Main

Let 2ndstreetpropertymanagement handle the complexity

At 2ndstreetpropertymanagement, we built our property management approach for investors who think in terms of ROI, cash flow, and portfolio growth, not just rent collection. We understand that precise expense tracking is not a back-office task. It is a core investment discipline that directly affects your returns.

If you are managing multiple properties and finding that bookkeeping is consuming time you should be spending on acquisitions or tenant relationships, our team can help you build the systems and oversight that protect your deductions and keep your financials audit-ready. Learn how we support investors with property management built around financial clarity and long-term performance.

FAQ

What expenses can landlords deduct on Schedule E?

Landlords can deduct advertising, insurance, mortgage interest, repairs, maintenance, property taxes, management fees, utilities, and depreciation on Schedule E. Capital improvements are not immediately deductible but are recovered through depreciation over the asset’s useful life.

How often should landlords reconcile rental property accounts?

Monthly reconciliation is the recommended minimum. Catalyst CPA notes that annual-only reconciliation commonly results in losing 8 to 15 percent of legitimate deductions due to untracked or miscategorized transactions.

What is the best software for tracking rental property expenses?

QuickBooks Online is the most widely used tool for landlords managing multiple properties, offering Class and Location tracking for per-property P&L reporting. RentRedi combines expense tracking with rent collection and maintenance management in one platform, making it a strong choice for landlords who want an all-in-one solution.

What is the difference between a repair and a capital improvement?

A repair restores a property to its original condition and is fully deductible in the current tax year. A capital improvement adds value, extends the property’s useful life, or adapts it to a new use, and must be depreciated over time under IRS Regulation 1.263(a)-3.

Do landlords need to keep physical receipts for rental expenses?

Physical receipts are not required. The IRS accepts digital copies, and digitizing receipts immediately after purchase is the recommended practice since paper receipts fade within months. Store digital copies organized by property and expense category for fast retrieval.

Recommended

Comments