How to Perform Rental Property Due Diligence

- Rey Rey Rodriguez

- Jun 11

- 9 min read

Rental property due diligence is the structured process of verifying a property’s physical condition, financial viability, legal status, and operational factors before you finalize a rental investment. The industry term for this process is “investment due diligence,” and it applies to every acquisition regardless of price or market. Skipping or rushing it is the single most common reason investors overpay, inherit hidden liabilities, or watch projected cash flow evaporate within the first year. The due diligence period for residential properties typically lasts between 7 and 30 days after an offer is accepted. That window is your contractual right to confirm the property operates as a business, not just a home.

How to perform rental property due diligence: the full framework

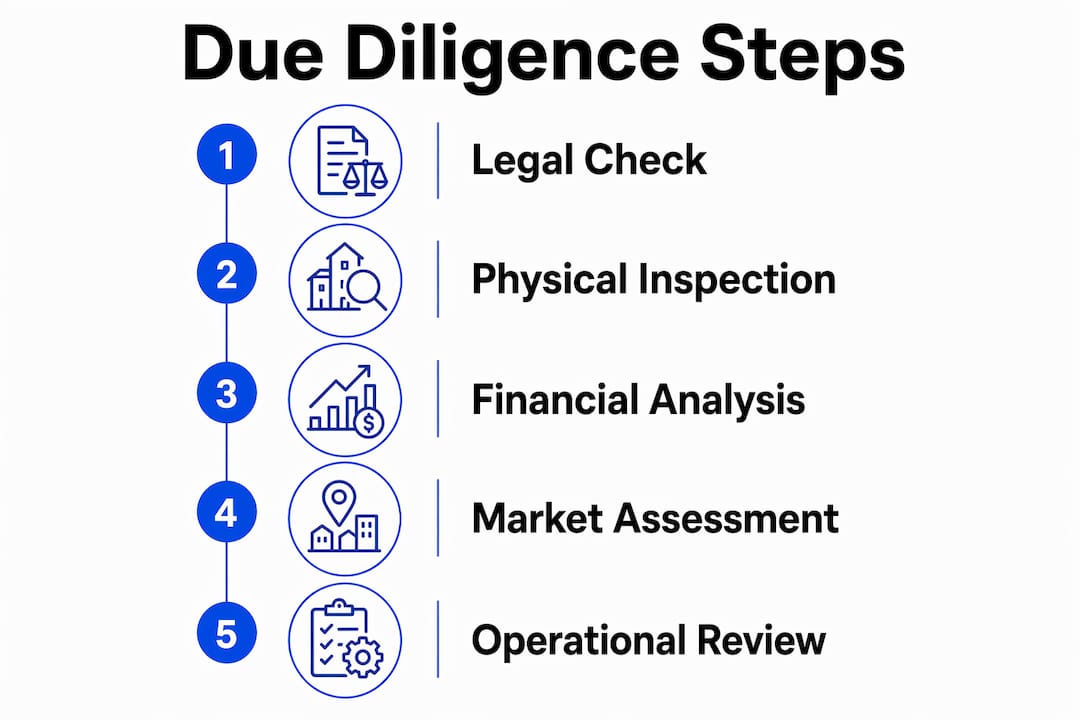

Rental property due diligence requires auditing physical, financial, legal, and operational systems to transform seller claims into verified facts. Think of it like buying a used car. You would never rely solely on the seller’s description of horsepower. You pull the vehicle history, run a mechanic’s inspection, and check the market value independently. The same logic applies here, but the stakes are far higher. A disciplined investor treats every acquisition as a business purchase, not a real estate transaction, and structures the due diligence process accordingly across four distinct pillars: legal, physical, financial, and operational.

How to verify ownership, legal status, and zoning compliance

Legal verification is the first pillar, and it must happen before you spend a dollar on inspections or analysis. A detailed title search by a title company reveals liens, easements, and encumbrances that can affect your ownership rights. Confirming the seller’s legal right to transfer the property is foundational. Without it, every other step in the process is built on sand.

Here is what to verify during legal due diligence:

Title search: Confirm no outstanding liens, tax judgments, or mechanic’s liens are attached to the property.

Easements and encumbrances: Identify any rights granted to utilities, neighbors, or municipalities that restrict your use of the land.

Zoning compliance: Confirm the property is zoned for residential rental use, and specifically for long-term versus short-term rentals if you plan to use platforms like Airbnb or VRBO.

Permits and rental registrations: Verify that any additions, conversions, or renovations were permitted. Unpermitted work can trigger costly remediation orders.

HOA restrictions: If the property is in a homeowners association, review CC&Rs for rental restrictions before closing.

Consult a real estate attorney and your local zoning office directly. Do not rely on the seller’s representations alone. Zoning rules for short-term rentals in particular have tightened significantly in cities like Denver, Nashville, and Austin since 2022, and what was legal two years ago may now require a special use permit.

What does a rental property inspection checklist cover?

Physical inspection is the second pillar, and it is where deals either get repriced or killed. Hire a licensed home inspector who has experience with investment properties, not just owner-occupied homes. The distinction matters because an investment-focused inspector will flag deferred maintenance patterns and estimate remaining useful life on major systems, not just document current defects.

Professional property inspections uncover issues like plumbing and electrical system problems that can create costly future repairs or make a property uninsurable. Two specific red flags deserve your attention: polybutylene plumbing, which was installed in millions of homes between 1978 and 1995 and is prone to catastrophic failure, and Federal Pacific electrical panels, which have a documented history of breaker failure and fire risk. Either finding should trigger a repair credit negotiation or a hard pass on the deal.

A thorough rental property inspection checklist covers:

Foundation and structure: Cracks, settling, water intrusion, and drainage issues

Roof: Age, condition, remaining life, and evidence of leaks or improper repairs

Electrical: Panel age and type, wiring condition, GFCI compliance, and load capacity

Plumbing: Pipe material, water heater age, water pressure, and drain function

HVAC: System age, filter condition, ductwork integrity, and service history

Windows and doors: Seals, locks, weatherproofing, and egress compliance

Environmental: Flood zone designation, asbestos in older properties, lead paint in pre-1978 construction

Pro Tip: Order a sewer scope inspection separately from the standard home inspection. Sewer line replacement costs between $3,000 and $15,000 depending on depth and material, and it is almost never included in a standard inspection report.

Use the inspection findings to get contractor estimates for every flagged item. Those numbers feed directly into your financial model and your repair credit negotiation with the seller.

How to verify rental income and analyze investment financials

Financial verification is the third pillar, and it is where most investors make their most expensive mistakes. Experienced investors verify seller financials against tax returns and bank statements because seller-reported income is often inflated by omitting vacancies and expenses. Request at least 24 months of bank statements, current leases, and the prior two years of Schedule E tax filings. Cross-reference reported rents against market comps using tools like Zillow and Rentometer.

The table below shows the key financial metrics every investor must calculate during due diligence:

Metric | Definition | Why It Matters |

Net Operating Income (NOI) | Gross rent minus all operating expenses, excluding debt service | Measures property profitability independent of financing |

Cap Rate | NOI divided by purchase price | Benchmarks value against comparable properties in the market |

Cash-on-Cash Return | Annual pre-tax cash flow divided by total cash invested | Measures actual return on your out-of-pocket capital |

DSCR | NOI divided by annual debt service | Lenders require 1.20 to 1.30 minimum for rental financing |

Vacancy Rate | Percentage of time the unit sits unoccupied | Investors should budget at least 8% as a baseline assumption |

Operating expenses are where pro forma projections most commonly diverge from reality. Budget for property taxes, insurance, utilities (if any are landlord-paid), property management at 8 to 10% of gross rents, vacancy at 8 to 10%, routine maintenance at 5 to 10% depending on property age, and a separate CapEx reserve. Capital expenditures are not annual expenses but irregular large costs that can wipe out years of cash flow, so a dedicated CapEx reserve of 5 to 10% of gross income is non-negotiable.

Pro Tip: Stress-test your cash flow model by running scenarios at 10% lower rent and 15% higher vacancy than your base case. If the deal still pencils at those numbers, you have a margin of safety. If it does not, you are relying on optimism, not analysis.

How to assess rental markets and local regulations

Market and regulatory research is the fourth pillar, and it directly determines tenant quality, legal exposure, and long-term profitability. Neighborhood factors like crime, school quality, and nearby employment significantly impact tenant quality and rental profitability. Wide-area crime statistics are insufficient. Use street-level tools like the Doorprofit crime map or NeighborhoodScout to evaluate the specific blocks surrounding the property, not just the zip code.

Beyond neighborhood fundamentals, review the following before closing:

Landlord-tenant laws: Understand your state and local rules on security deposit limits, required notice periods for entry and termination, and eviction procedures. States like California, New York, and Oregon have tenant-friendly statutes that materially affect operating costs.

Rent control and stabilization: Confirm whether the property falls under any rent increase restrictions. Some cities apply rent stabilization to properties based on age or unit count.

Short-term rental regulations: If you plan to operate on Airbnb or VRBO, confirm local licensing requirements, owner-occupancy rules, and any HOA prohibitions before assuming that revenue model.

Landlord insurance: Landlord insurance differs from homeowners insurance and is necessary to protect against renter-related damages and liabilities. Obtain quotes before closing to include the actual premium in your expense model.

If you are purchasing an occupied property, tenant screening becomes part of due diligence. Review existing lease terms, payment history, and any open disputes. Inheriting a non-paying tenant or a lease below market rate affects your returns from day one.

Self-management vs. professional management: what investors miss

Operational due diligence is the step most investors skip entirely, and it is the one that determines whether your investment performs as modeled. The decision to self-manage or hire a property manager is not just a cost question. It is a capacity and risk question that affects your vacancy rate, maintenance response time, and legal compliance.

Self-managing investors frequently underestimate the time cost of tenant communications, maintenance coordination, lease renewals, and move-in and move-out inspections. Well-documented, signed inspection checklists at move-in and move-out protect landlords during security deposit disputes and help enforce tenant responsibilities. Without a system for this, you are exposed in every dispute. Professional property managers bring systems, vendor networks, and legal compliance infrastructure that most individual investors cannot replicate at scale.

Budget 8 to 10% of gross rents for professional management even if you plan to self-manage initially. This keeps your financial model honest and makes the transition to professional management seamless if your portfolio grows. The self-management challenges that trip up investors most often involve maintenance coordination and tenant screening, both of which compound quickly when you own multiple units.

Key takeaways

Successful rental property investing depends on verifying physical condition, legal status, financial performance, and operational readiness before you close, not after.

Point | Details |

Legal verification comes first | Confirm title, zoning, and permits before spending on inspections or analysis. |

Inspections protect your capital | Hire an investment-focused inspector and order a separate sewer scope to catch costly hidden defects. |

Verify financials independently | Cross-reference seller income claims against tax returns, bank statements, and market comps from Zillow and Rentometer. |

Budget conservatively for expenses | Use 8 to 10% vacancy, 8 to 10% management, and a separate CapEx reserve of 5 to 10% of gross income. |

Operational planning is non-negotiable | Decide on management structure before closing and build its cost into your financial model from day one. |

The due diligence lesson most investors learn the hard way

I have reviewed hundreds of rental property deals over the years, and the pattern is consistent. Investors who skip or rush due diligence do not just buy bad properties. They buy good properties at the wrong price with the wrong assumptions baked in. The seller’s pro forma is a marketing document. It is not a financial model.

The most expensive mistake I see is trusting seller-reported expenses without verification. A seller who self-manages and never accounts for vacancy, CapEx, or management fees will show you a net income number that looks compelling. Run those same numbers with realistic expense assumptions and the deal often falls apart. That is not a bad outcome. That is due diligence working exactly as it should.

Build your team before you need them. A reliable title company, a licensed inspector who knows investment properties, a real estate attorney familiar with landlord-tenant law in your target market, and a CPA who understands Schedule E reporting will save you far more than their fees. The investors who consistently avoid costly rental mistakes are not smarter than everyone else. They are more disciplined about the process.

— Main

Work with a property management team built for investors

Conducting thorough due diligence is only the beginning. Once you close, the operational work starts, and that is where returns are either protected or eroded. 2ndstreetpropertymanagement was built by investors for investors, which means the team understands what matters: verified tenant screening, accurate rent collection, proactive maintenance, and financial reporting that actually reflects your investment performance.

Whether you are evaluating your first rental or scaling a portfolio, 2ndstreetpropertymanagement provides the property management infrastructure to protect your due diligence work after closing. From tenant screening to lease compliance and maintenance coordination, the team handles the operational details so your numbers stay on track. Reach out to 2ndstreetpropertymanagement to explore how professional management can support your investment goals.

FAQ

What is rental property due diligence?

Rental property due diligence is the structured process of verifying a property’s physical condition, financial performance, legal status, and operational factors before finalizing a purchase. The standard due diligence period lasts between 7 and 30 days after an offer is accepted.

What should a rental property inspection checklist include?

A rental property inspection checklist should cover the foundation, roof, electrical panel, plumbing type, HVAC systems, windows, and environmental hazards like flood zone status and lead paint. A separate sewer scope inspection is also recommended for any property over 20 years old.

How do I verify rental income during due diligence?

Request at least 24 months of bank statements, current signed leases, and two years of Schedule E tax filings from the seller. Cross-reference reported rents against market data from tools like Zillow and Rentometer to confirm income claims are accurate.

What DSCR do lenders require for rental property financing?

Most lenders require a Debt Service Coverage Ratio of 1.20 to 1.30 or higher for rental property loans. A DSCR below 1.0 means the property’s income does not cover its debt payments, which signals negative monthly cash flow.

Should I self-manage or hire a property manager after closing?

Budget for professional property management at 8 to 10% of gross rents regardless of your initial plan, because it keeps your financial model realistic and gives you a clear baseline for evaluating self-management costs. The decision depends on your time, experience, and portfolio size.

Recommended

Comments