How to Buy Rentals: A 2026 Investor's Guide

- Rey Rey Rodriguez

- 27 minutes ago

- 7 min read

Buying rental properties means acquiring real estate that generates monthly income and builds long-term wealth through appreciation, debt paydown, and depreciation. The industry term is income property investing, and it rewards investors who treat each purchase as a business decision rather than a lifestyle choice. Success depends on three things: choosing the right property type, financing it correctly, and managing it like an operator. Whether you are looking at a single-family home or a small multifamily building, the fundamentals of how to buy rental income properties remain the same. Conventional loans, FHA house hacking, and DSCR loans each open different doors depending on your situation.

What property types are best for rental investments?

Single-family homes and small multifamily properties (duplexes through fourplexes) are the two most practical entry points when you purchase rental properties for the first time. Single-family homes are easier to finance, attract long-term tenants, and carry lower management complexity. Small multifamily buildings generate more income per purchase, spread vacancy risk across multiple units, and qualify for residential financing up to four units.

Location, condition, and bedroom count drive tenant demand more than any other variables. A three-bedroom, two-bathroom home in a neighborhood with good schools and low vacancy will outperform a larger property in a declining area every time. Prioritize properties that are move-in ready or need only light cosmetic work. Major structural repairs eat your reserves before you collect a single rent check.

The most disciplined investors build a buy box before they search a single listing. A buy box is a written set of criteria: target market, price range, property type, minimum bedroom count, and required cash flow metrics. Standardizing your buy box prevents emotional decisions and keeps your acquisition process focused. Think of it like a hiring rubric. You would not interview candidates without knowing the job requirements first.

Two benchmarks every investor needs to know are the 1% rule and cap rate. The 1% rule states that monthly rent should equal at least 1% of the purchase price. A $200,000 property should rent for at least $2,000 per month. Cap rate benchmarks typically range 5%–8%, and most investors target $150–$200 in monthly net cash flow per unit after all expenses. These numbers are filters, not guarantees. Use them to eliminate weak deals quickly.

Pro Tip: Run your numbers with a 5%–10% vacancy assumption and a 1% annual maintenance budget before you make any offer. Properties that only cash flow under perfect conditions will drain you the moment a tenant moves out.

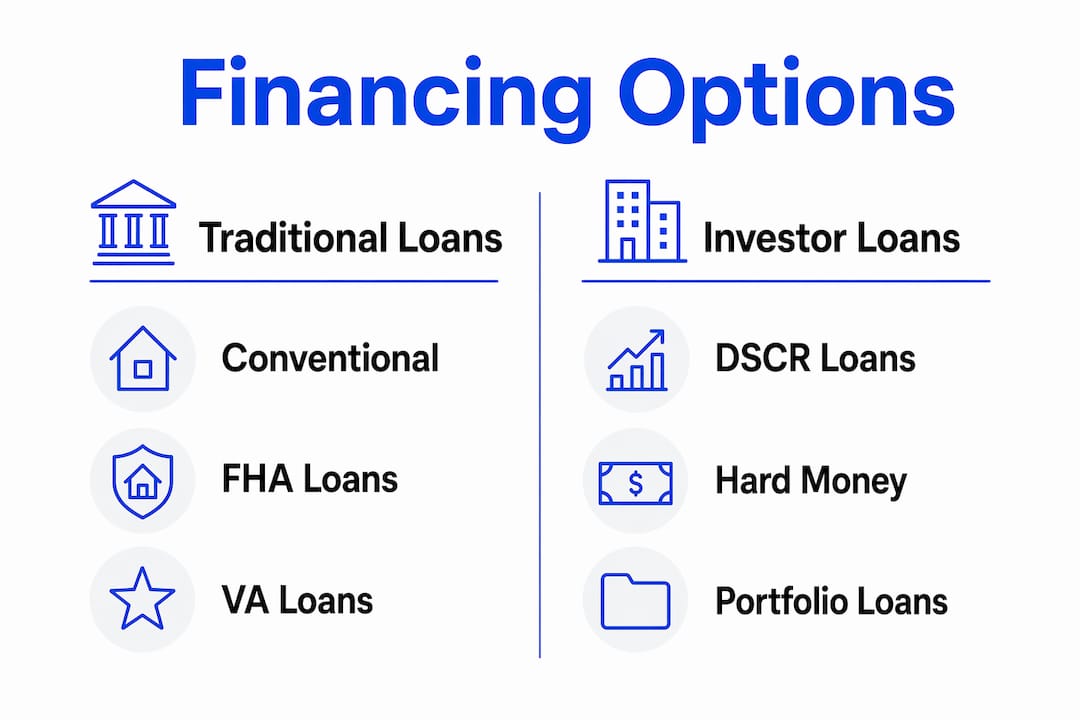

How do you finance a rental property purchase in 2026?

Financing is where most new investors make their most expensive mistakes. Conventional investment loans require 20%–25% down with 2%–4% in closing costs, and lenders charge rates 0.5%–0.75% higher than primary residence loans. On a $200,000–$250,000 purchase, total cash needed can range from $32,500 to $65,000. That number surprises most first-time buyers. Budget for it before you start shopping.

FHA loans offer a lower barrier to entry for house hacking. If you buy a duplex, triplex, or fourplex and live in one unit, FHA financing allows as little as 3.5% down. The rental income from the other units offsets your mortgage payment. This is one of the most effective ways for families to start building a rental portfolio without a large cash reserve.

DSCR loans (Debt Service Coverage Ratio loans) are the tool of choice for investors who want to buy under an LLC or who have complex personal income. DSCR loans qualify based on the property’s rental income rather than the borrower’s W-2 or tax returns. The lender calculates whether the rent covers the mortgage payment at a ratio of 1.0 or higher. Minimum loan amounts typically start at $100,000–$125,000, and lenders require 25% down plus six months of reserves.

Loan Type | Down Payment | Qualifies On | Best For |

Conventional | 20%–25% | Personal income | W-2 investors, first purchase |

FHA (house hack) | 3.5% | Personal income | Owner-occupant multifamily |

DSCR | 25% | Rental income | LLC buyers, self-employed |

Pro Tip: Never assume your first tenant will pay top-of-market rent. Model your cash flow at 90%–95% of the current market rent to build in a buffer from day one.

Step-by-step process to buy rental properties

A clear process separates investors who close profitable deals from those who spend months spinning their wheels. Follow these steps in order.

Define your buy box. Set your target market, price range, property type, and minimum cash flow requirements before you open Zillow or Realtor.com. Without this filter, every listing looks like an opportunity.

Research your target market. Use price-to-rent ratios to identify markets where rents support positive cash flow. A market where median home prices are $200,000 and median rents are $1,800 is more favorable than one where prices are $400,000 and rents are $2,200. Tools like Rentometer give you real-time rent comparables by zip code.

Assemble your team. Find an investor-friendly real estate agent who owns rental properties themselves. Pair them with a lender who specializes in investment financing, whether conventional, FHA, or DSCR. A good lender pre-approves you with speed and accuracy, which matters when you are competing for deals.

Analyze deals before you tour them. Run the numbers on paper first. Calculate gross rent, subtract vacancy (5%–10%), subtract operating expenses (taxes, insurance, maintenance, management), and subtract your mortgage payment. If the deal does not pencil on paper, do not visit the property. Visiting creates emotional attachment.

Make data-backed offers. Sellers prioritize certainty and speed over the highest price. A clean offer with a 21–30 day closing timeline, an inspection contingency, and a financing contingency is often stronger than a higher bid with unclear terms. Ask for seller concessions to cover closing costs when the market allows it.

Conduct due diligence. Hire a licensed inspector. Review utility bills, rent rolls if the property is already occupied, and local rental regulations. Verify that the actual rent matches what the seller claims.

Close and place a tenant. At closing, confirm your property management plan. If you self-manage, review rental property showing best practices before your first showing. If you hire a manager, have them in place before you close so tenant placement starts immediately.

Common mistakes when purchasing rental properties

The most expensive mistake in real estate rental purchases is buying with your gut instead of your buy box. Emotional buying looks like this: you tour a property, you love the neighborhood, and you convince yourself the numbers will work out. They rarely do. Rental investing succeeds when you treat acquisition as a repeatable, criteria-driven process.

Underestimating reserves is the second most common failure point. Budget six months of expenses beyond your down payment and closing costs. That reserve covers a vacancy period, a water heater replacement, or an HVAC repair without forcing you to dip into personal savings. New landlords who skip this step often sell their first property at a loss within two years.

Three other pitfalls to avoid:

Ignoring vacancy. A property that cash flows at 100% occupancy is not a cash-flowing property. Model vacancy at 5%–10% every year.

Using optimistic rent assumptions. Rent what the market will bear today, not what you hope it will bear next year.

Mishandling LLC contracts. An LLC can be named on a contract before it is formally registered, but it must be fully formed by closing. Misnaming the LLC causes delays and can kill your financing.

“Rental property investing is an operational business. The investors who build wealth are the ones who think like operators, not shoppers.”

Pro Tip: Use a cash flow analysis tool to stress-test every deal before you make an offer. Run three scenarios: best case, base case, and worst case.

Key takeaways

Buying rental properties builds long-term wealth when you combine a defined buy box, disciplined financing, and an operator’s mindset from day one.

Point | Details |

Define your buy box first | Set location, price, property type, and cash flow criteria before searching any listings. |

Match financing to your situation | Conventional loans suit W-2 buyers; DSCR loans serve LLC owners and self-employed investors. |

Reserve six months of expenses | Budget reserves beyond closing costs to cover vacancies and unexpected repairs. |

Use data-backed offers | Fast closings with contingencies beat higher prices when sellers prioritize certainty. |

Think like an operator | Sustainable cash flow comes from standardized criteria, not emotional or speculative buying. |

Why slow and steady wins in rental investing

Most investors I work with want to scale fast. They see portfolios of 10 or 20 properties and assume speed is the goal. My experience tells a different story. The investors who build real, lasting wealth are the ones who buy one or two properties per year, get them stabilized, and let compounding do the work.

Long-term buy-and-hold investing remains the most reliable path to wealth over 20–30 years compared to speculative flipping or rapid leveraged scaling. A 30-year mortgage at 7% is not a problem if the asset is well-priced and the rent covers the payment. Rates can be refinanced when conditions improve. The equity, the depreciation, and the debt paydown keep compounding regardless.

The investors who struggle are the ones who confuse movement with progress. They buy three properties in one year, stretch their reserves thin, and hit a wall when one unit sits vacant for 60 days. Slow, deliberate growth with strong cash flow fundamentals is not a conservative strategy. It is the most effective one. Build your long-term wealth strategy around assets that perform in bad markets, not just good ones.

— Main

How 2ndstreetpropertymanagement helps rental investors succeed

2ndstreetpropertymanagement was built by investors for investors. The team understands that your rental property is not just a home. It is a business asset that needs to perform.

Whether you are buying your first rental unit or adding to an existing portfolio, 2ndstreetpropertymanagement offers reliable property management services designed to protect your cash flow and reduce your workload. From tenant placement to maintenance coordination, the team handles the operational side so you can focus on your next acquisition. Explore the full range of resources and services at 2ndstreetpropertymanagement.com and put your portfolio on a stronger footing today.

FAQ

What is the minimum down payment to buy a rental property?

Conventional investment loans require 20%–25% down. FHA loans allow 3.5% down if you live in one unit of a multifamily property (house hacking).

What is a DSCR loan and who should use it?

A DSCR loan qualifies based on the property’s rental income rather than your personal income. It is the best option for LLC buyers, self-employed investors, and anyone with complex tax returns.

How much cash do I need beyond the down payment?

Budget 2%–4% of the purchase price for closing costs, plus six months of operating expenses as reserves. Skipping reserves is the most common reason new landlords sell at a loss.

What is the 1% rule in rental investing?

The 1% rule states that monthly rent should equal at least 1% of the purchase price. A $200,000 property should generate at least $2,000 per month in rent to meet this benchmark.

Should I buy rental properties under an LLC?

An LLC provides liability protection and works well with DSCR financing. If you use an LLC on the purchase contract, make sure it is fully registered before closing day to avoid delays.

Recommended

Comments