Cash Flow for Landlords: Maximize Your Rental Returns

- Rey Rey Rodriguez

- 1 day ago

- 8 min read

Cash flow is defined as the net movement of actual dollars into and out of your rental property after every expense is paid. It is the single most reliable indicator of whether your investment is working for you or against you. Profit on paper means nothing if your bank account runs dry between rent checks. Landlords who master cash flow management protect their income, reduce risk, and build wealth that compounds over time. This guide covers the components, calculations, strategies, and tools you need to take full control of your rental property finances.

What is cash flow in rental property investing?

Cash flow in real estate is the money left over after all property-related expenses are subtracted from all income received. It is not the same as profit. Profitability and cash flow are distinct: a property can show a net gain on your tax return while your checking account sits empty because a tenant paid late or a repair bill arrived before rent did. That timing gap is where landlords get into trouble.

Positive cash flow means your rental income exceeds your total outflows each month. Negative cash flow means the opposite. Free cash flow refers to what remains after capital expenditures like roof replacements or HVAC upgrades. Understanding which type you are dealing with at any given moment is the foundation of sound real estate investing.

Cash flow management is not a quarterly task. It requires proactive and continuous attention to stay ahead of vacancies, repairs, and market shifts. Landlords who treat it as a one-time calculation confuse movement with progress. The investors who build lasting portfolios are the ones who monitor their numbers weekly, not annually.

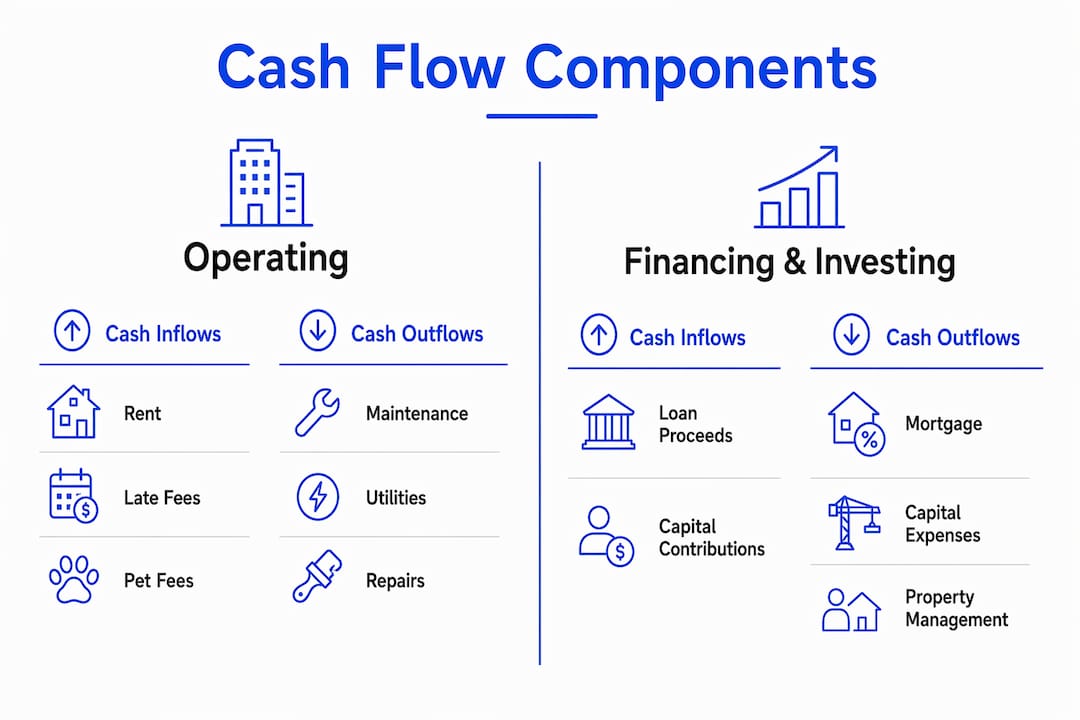

What are the key components of rental property cash flow?

Every dollar moving through your rental property falls into one of three categories: operating, investing, or financing. Operating cash flow covers your day-to-day income and expenses. Investing cash flow covers property purchases, sales, and capital improvements. Financing cash flow covers mortgage payments, loan draws, and interest.

The table below breaks down the most common components landlords track:

Category | Cash Inflows | Cash Outflows |

Operating | Rent, late fees, pet fees | Maintenance, insurance, property taxes, utilities, management fees |

Investing | Property sale proceeds, depreciation recapture | Renovations, new property purchases, major capital improvements |

Financing | Loan draws, refinance proceeds | Mortgage principal, interest payments, loan origination fees |

Operating cash flow is the most telling number for day-to-day health. A property that generates strong rent but carries a heavy mortgage and deferred maintenance can still produce negative operating cash flow. Tracking all three categories separately gives you a complete picture instead of a misleading summary.

Common inflows to monitor include:

Monthly rent from all units

Late payment fees

Pet deposits and monthly pet rent

Parking or storage fees

Laundry income on multi-unit properties

Common outflows that landlords underestimate include property management fees, vacancy costs, turnover expenses, and capital reserves. Ignoring any one of these will distort your analysis and lead to poor decisions.

How do landlords calculate and analyze cash flow accurately?

The basic formula is straightforward: total cash inflows minus total cash outflows equals net cash flow. The challenge is not the math. The challenge is capturing every inflow and outflow with precision and accounting for timing.

Here is a practical four-step process for accurate cash flow analysis:

List all income sources. Include base rent, ancillary fees, and any other recurring revenue. Use your rental property cash flow tool to centralize this data rather than tracking it across spreadsheets.

Categorize every expense. Separate fixed costs like mortgage and insurance from variable costs like repairs and utilities. Variable costs are where most landlords underestimate their outflows.

Account for timing. Rent collected on the 5th of the month does not help you if your mortgage drafts on the 1st. Map the actual dates, not just the amounts.

Build in reserves. A 60–90 day operating expense reserve protects you from a single bad month turning into a financial crisis. Fund this account before you deploy excess cash elsewhere.

Tracking metrics like days sales outstanding gives you visibility into how quickly tenants actually pay versus when rent is due. That gap directly affects your liquidity. A tenant who consistently pays five days late creates a predictable shortfall you can plan around. One who pays 30 days late creates a crisis.

Pro Tip: Run a rolling 3–6 month cash flow forecast and update it with actual results every week. This practice, recommended by Stripe’s small business research, lets you spot shortfalls weeks before they hit your account rather than discovering them after the fact.

For a deeper look at the tools that support this kind of analysis, the guide on cash flow analysis tools covers the leading software options built specifically for real estate investors.

What strategies improve cash flow for rental property owners?

Improving your net cash position requires working both sides of the equation: increasing inflows and reducing outflows. The most effective landlords do both simultaneously rather than focusing on one at the expense of the other.

Tighten rent collection. Offer a small discount for early payment or automate rent collection through platforms like Buildium or AppFolio. Late payments are the most common cause of short-term cash shortfalls.

Renegotiate vendor contracts annually. Landscaping, pest control, and maintenance contracts often carry built-in price increases. Reviewing them each year and getting competitive bids keeps your expense line honest.

Maintain a reserve fund. A 60–90 day cash reserve is not optional. It is the difference between a manageable repair bill and a forced sale.

Review your budget quarterly. Markets shift. Insurance premiums rise. Property taxes get reassessed. A budget that was accurate in January may be dangerously off by October.

Use property management software. Tools like Rentec Direct, Propertyware, or Buildium give you real-time visibility into income, expenses, and vacancy rates. Weekly forecasts are more effective than monthly reviews during periods of growth or market volatility.

Establish a flexible credit line. A business line of credit gives you a buffer for unexpected expenses without disrupting your reserve fund. Use it as a bridge, not a crutch.

Pro Tip: Do not wait until a unit turns over to review your rent pricing. Check comparable rents in your market every six months and adjust at lease renewal. Even a $75 monthly increase on a single unit adds $900 annually to your operating cash flow.

The guide on self-management challenges covers additional pitfalls that erode positive cash flow for landlords who manage their own properties.

What causes negative cash flow and how do you fix it?

Negative cash flow occurs when outflows exceed inflows. This is distinct from profitability. A property can depreciate on paper for tax purposes while simultaneously draining your bank account. Negative operating cash flow is the most serious type because it signals a structural problem with your income or expense base.

The table below maps the most common causes to their practical remedies:

Cause | Remedy |

Tenant late payments | Automate collection, enforce late fees consistently |

High vacancy rates | Improve marketing, review pricing, reduce turnover time |

Unexpected repairs | Fund a capital reserve account, schedule preventive maintenance |

Rising insurance or taxes | Shop coverage annually, appeal tax assessments when justified |

Over-leveraged financing | Refinance to lower rate or extend amortization period |

Deferred maintenance costs | Create a 12-month maintenance calendar and budget accordingly |

Not all negative cash flow signals a problem. Negative cash flow can be an intentional strategy during expansion phases when you are renovating a property to increase its rent potential or acquiring new assets. The key distinction is whether your operating cash flow remains positive while your investing cash flow is temporarily negative. If both are negative at the same time, that requires immediate attention.

Early warning signs show up in your forecast before they hit your account. Only 24% of U.S. small-business owners felt very comfortable with their cash flow in Q4 2025, down from 31% the prior quarter. That decline reflects how quickly market conditions can shift your financial position. Landlords who run weekly forecasts catch these shifts early. Those who review monthly often react too late.

Key Takeaways

Consistent cash flow management is the most reliable path to sustainable rental income and long-term investment returns.

Point | Details |

Cash flow vs. profit | A property can be profitable on paper while running short on actual cash due to timing gaps. |

Reserve fund requirement | Keep 60–90 days of operating expenses in reserve before deploying excess cash elsewhere. |

Forecast frequency | Update your rolling 3–6 month cash flow forecast weekly to catch shortfalls before they hit. |

Negative cash flow context | Negative investing cash flow during renovations is strategic. Negative operating cash flow is a warning sign. |

Expense discipline | Review vendor contracts, insurance, and rent pricing every six months to protect your margins. |

Cash flow is the heartbeat of your portfolio

I have reviewed hundreds of rental property portfolios over the years, and the pattern is consistent. The investors who struggle are rarely the ones with bad properties. They are the ones with good properties and poor financial visibility. They know their rent roll. They do not know their actual net cash position on any given Tuesday.

The conventional wisdom says to focus on appreciation and let the numbers work themselves out over time. That advice is incomplete. Appreciation builds wealth on paper. Cash flow keeps you solvent while you wait for it. A property that bleeds $500 a month for five years costs you $30,000 in real dollars before appreciation delivers a single cent of realized gain.

What I recommend is treating your cash flow forecast the same way a pilot treats an instrument panel. You do not check it once before takeoff and assume everything is fine. You monitor it continuously and adjust when readings change. Only 6% of finance and accounting leaders have the full capabilities to execute their financial priorities. That gap is an opportunity for landlords who commit to building this skill.

Modern tools make this easier than it has ever been. Buildium, AppFolio, and Rentec Direct all offer real-time dashboards that replace the spreadsheet guesswork most landlords still rely on. The investors who adopt these tools and review their numbers weekly are the ones who stay liquid, stay confident, and keep growing their portfolios when others are forced to sell.

— Main

How 2ndstreetpropertymanagement helps you protect your rental income

Managing cash flow across multiple rental properties is demanding work. 2ndstreetpropertymanagement was built by investors who understand that reality firsthand.

2ndstreetpropertymanagement offers property management services designed to protect your income at every point in the rental cycle, from tenant screening and rent collection to expense tracking and financial reporting. The team handles the operational details that drain your time and erode your margins, so you can focus on growing your portfolio. If you are ready to take control of your rental property finances, explore how 2ndstreetpropertymanagement’s services can give you the visibility and support your investment deserves.

FAQ

What is the cash flow formula for rental properties?

Net cash flow equals total rental income minus all operating expenses, mortgage payments, and capital reserves. The formula is simple; the discipline is in capturing every expense accurately.

How much cash flow should a rental property generate?

Most experienced investors target a minimum of $100–$200 per unit per month in net cash flow after all expenses. The right number depends on your market, financing structure, and risk tolerance.

What is the difference between free cash flow and operating cash flow?

Operating cash flow covers income and expenses from running the property day to day. Free cash flow subtracts capital expenditures like major renovations or equipment replacement, giving you a clearer picture of what is truly available.

How do I fix negative cash flow on a rental property?

Start by identifying whether the problem is income-side (low rent, high vacancy) or expense-side (deferred maintenance, over-leveraged debt). Address the root cause directly rather than covering shortfalls with credit. A cash flow analysis will pinpoint where the leak is.

How often should landlords review their cash flow forecast?

Weekly forecasts are more effective than monthly reviews, especially during periods of market volatility or portfolio growth. Update your forecast with actual results each week to stay ahead of potential shortfalls.

Recommended

Comments