The Role of Rental Income Reporting for Landlords

- Rey Rey Rodriguez

- 1 day ago

- 8 min read

Rental income reporting is defined as the process of declaring all rental earnings to the IRS, primarily through Schedule E of Form 1040, to meet federal tax obligations and document financial activity. The role of rental income reporting extends well beyond basic compliance. It determines which deductions you can legally claim, how lenders assess your borrowing capacity, and whether your investment records hold up under audit. Landlords who treat this process as a routine administrative task often leave significant money on the table. Those who treat it as a financial discipline protect their wealth, reduce their tax burden, and build the credibility that serious real estate investing demands.

What is the role of rental income reporting for tax compliance?

Rental income reporting is the foundation of your tax position as a landlord. The IRS requires you to report all rental earnings, and residential rental income is reported on Schedule E (Form 1040). Schedule E captures your gross rents received alongside allowable deductions such as mortgage interest, property taxes, repairs, insurance, and depreciation.

Depreciation is the detail most landlords underestimate. The IRS mandates straight-line depreciation over 27.5 years using the Modified Accelerated Cost Recovery System (MACRS GDS) for residential rental property. Depreciation is mandatory, even if you never claim it. If you skip it, the IRS still adjusts your property’s cost basis as if you had taken it, which inflates your capital gains tax when you sell.

Rental income is taxed at your marginal rate, ranging from 10% to 37%, but it is not subject to self-employment tax unless you provide substantial services to tenants. That distinction matters for your net tax liability. Passive loss rules allow active participants with a modified adjusted gross income (AGI) under $100,000 to deduct up to $25,000 in rental losses annually. That allowance phases out completely at $150,000 AGI.

One important exception: if you rent your property for fewer than 15 days in a year, you do not report that income and cannot deduct related expenses. Real estate professionals who meet IRS hour requirements can treat rental losses as non-passive, which removes the AGI cap entirely.

Pro Tip: Classify every expense as either a repair or an improvement before you file. Repairs are deductible immediately. Improvements must be capitalized and depreciated. The de minimis safe harbor lets you expense items costing up to $2,500 each, which keeps small improvement costs off your depreciation schedule.

Why does rental income documentation matter so much?

Accurate documentation is what separates a defensible tax return from an expensive audit. The IRS requires landlords to maintain records for all income and expenses under IRC Section 6001. Poor recordkeeping leads directly to disallowed deductions, accuracy-related penalties up to 20%, and added taxes with interest.

The documents you need to retain include:

Lease agreements for every tenant, signed and dated

Bank statements showing rent deposits that match reported income

Receipts and invoices for every repair, maintenance expense, and capital improvement

1099 forms received from payment processors or issued to contractors

Depreciation schedules showing the cost basis and accumulated depreciation for each asset

Mileage logs if you drive to the property for management purposes

Retention periods matter. The IRS generally has three years to audit a return, but that window extends to six years if you underreport income by more than 25%. Records related to your property’s cost basis, including the original purchase price and all capital improvements, should be kept permanently. You will need that basis history to calculate your gain when you eventually sell.

IRS examiners prioritize contemporaneous documents created at the time of the transaction. A receipt dated the same day as the repair carries far more weight than a reconstructed expense list prepared during an audit. Digital tools that timestamp uploads and sync with your bank feed create that contemporaneous record automatically.

Pro Tip: Reconcile your rental income and expense records monthly, not at tax time. A monthly reconciliation catches missing receipts while the transaction is still fresh. It also makes rental property bookkeeping a 20-minute task instead of a two-day scramble every April.

How does rental income reporting affect your lending power?

Lenders treat your Schedule E as the primary proof of rental income when you apply for a mortgage or investment property loan. They verify rental income using Schedule E, signed leases, and bank deposit records. If those three sources do not align, underwriters exclude the income entirely from their calculations. That exclusion can kill a loan approval or force you into a higher rate.

The consistency of your documentation directly shapes your borrowing capacity. Common pitfalls that landlords face include:

Unreported cash rent that appears in bank deposits but not on Schedule E, creating an unexplained discrepancy

Expenses that exceed income without proper documentation, which raises underwriter flags

Missing lease agreements for current tenants, leaving lenders without the contractual basis to count that income

Short-term rental income reported inconsistently across platforms and tax returns

Documentation Type | What Lenders Verify | Risk if Missing |

Schedule E (Form 1040) | Gross rents and net income after expenses | Income excluded from underwriting |

Signed lease agreements | Lease term, rent amount, and tenant identity | Income treated as unverified |

Bank deposit statements | Actual rent received matches reported amounts | Discrepancy triggers income exclusion |

Rent ledger | Payment history for new or recently rented properties | No income history to underwrite |

For newly acquired properties or recent tenants, a formal rent ledger fills the gap. A clean rent ledger tracks each payment’s date, amount, and method, and it must align with the lease terms and bank deposits. Debt Service Coverage Ratio (DSCR) loans, which are common for investment properties, rely heavily on this ledger when tax returns do not yet reflect the property’s income history.

Short-term rental income from platforms like Airbnb or VRBO adds another layer. Third-party payment processors report gross earnings directly to the IRS. That means the IRS sees your rental income even if you do not report it, which removes any ambiguity about your disclosure obligations.

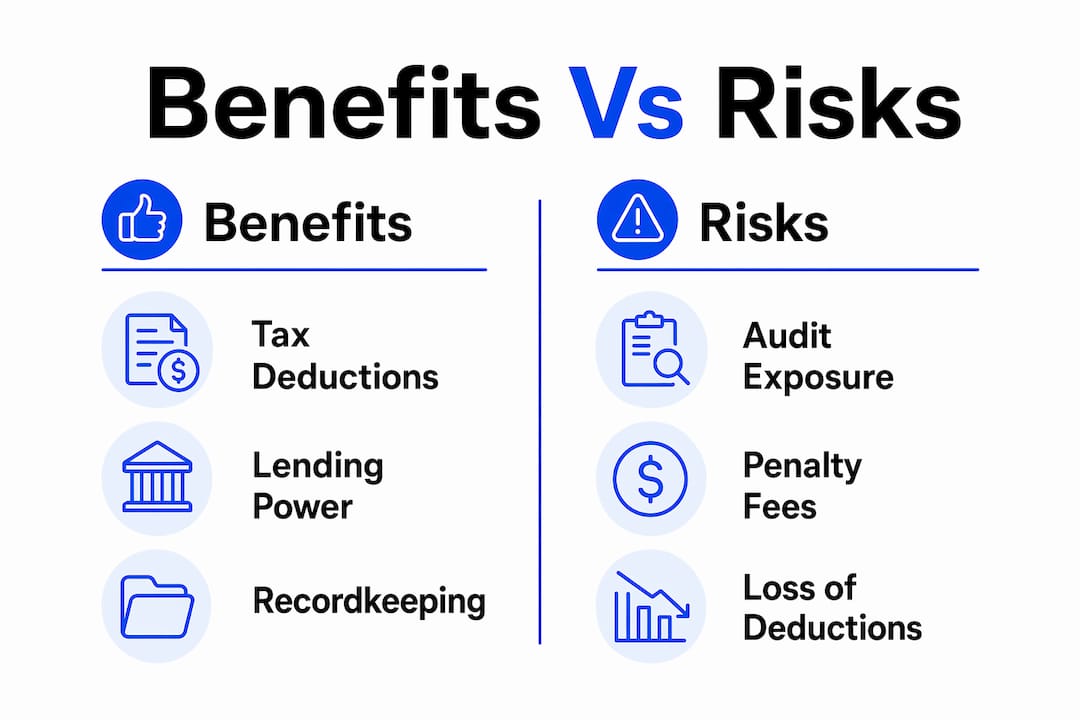

What are the real benefits and risks of reporting rental income correctly?

Proper rental income reporting delivers concrete financial advantages. Landlords who report accurately can claim deductions for mortgage interest, property taxes, insurance, repairs, professional fees, and depreciation. The combination of depreciation and passive loss allowances can reduce or eliminate taxable income on a cash-flowing property. That is a legal tax benefit that only exists when your records support it.

The risks of incorrect or incomplete reporting are equally concrete. Unreported rental income eliminates your ability to deduct any expenses against that income. The IRS can assess back taxes, interest, and a 20% accuracy-related penalty on the underpayment. In cases of willful non-disclosure, the exposure is significantly greater.

Category | Benefit of Correct Reporting | Risk of Incorrect Reporting |

Tax deductions | Depreciation, repairs, and interest fully deductible | All deductions disallowed on unreported income |

Audit exposure | Clean records reduce audit risk and resolve it quickly | Poor records invite penalties and added assessments |

Lending | Income counts toward borrowing capacity | Inconsistent records exclude income from underwriting |

Wealth protection | Maximizes after-tax returns on investment | Inflated capital gains at sale from missed depreciation |

Recordkeeping functions as a wealth-protection asset, not just an administrative requirement. Landlords who maintain clean books protect their deductions, simplify any audit, and build the financial credibility that supports portfolio growth. The landlords who treat documentation as optional are the ones who pay the most at tax time and qualify for the least when they want to buy their next property.

Pro Tip: Review your rental property tax strategy with a CPA who specializes in real estate before year-end, not after. A mid-year review lets you accelerate repairs, time capital improvements, and plan around passive loss thresholds while you still have time to act.

Key Takeaways

Accurate rental income reporting protects your deductions, strengthens your lending position, and shields your investment returns from IRS penalties and inflated capital gains.

Point | Details |

Report on Schedule E | All residential rental income and expenses belong on Schedule E of Form 1040. |

Claim depreciation every year | Depreciation is mandatory; skipping it inflates your capital gains tax at sale. |

Document every transaction | IRS Section 6001 requires records for all income and expenses; retain basis records permanently. |

Align your income sources | Schedule E, leases, and bank deposits must match for lenders to count your rental income. |

Unreported income costs more | Failing to report eliminates all related deductions and triggers accuracy-related penalties up to 20%. |

Why I think most landlords underestimate what reporting actually protects

Most landlords think about rental income reporting as a tax obligation. They file Schedule E because they have to, not because they understand what it protects. That framing is where the real cost hides.

The landlords I have seen struggle most are not the ones who cheat the system. They are the ones who are sloppy. They deposit rent in personal accounts. They pay contractors in cash without receipts. They skip depreciation because it seems complicated. Then they apply for a refinance and discover their income does not qualify, or they sell a property and face a capital gains bill they never anticipated because their basis was never properly tracked.

Recordkeeping is not paperwork. It is the documentation of your financial position. Every receipt you keep is a deduction you can defend. Every depreciation schedule you maintain is a future tax liability you can calculate and plan around. The expense tracking discipline that feels tedious in year one becomes the competitive advantage that lets you refinance, expand, and sell on your terms in year ten.

The landlords who build real wealth treat their rental portfolio like a business. That means monthly reconciliations, organized digital records, and a tax strategy reviewed before December 31, not after April 15. The IRS is not your biggest threat. Your own disorganization is.

— Main

How 2ndstreetpropertymanagement supports your rental income reporting

Rental income reporting gets complicated fast, especially when you own multiple properties, mix short-term and long-term rentals, or are scaling your portfolio.

2ndstreetpropertymanagement is built by investors for investors, which means the team understands what landlords actually need: organized income and expense records, consistent documentation that satisfies both the IRS and lenders, and a management approach that keeps your financial records clean year-round. From rent collection tracking to expense documentation, 2ndstreetpropertymanagement helps you maintain the paper trail that protects your deductions and supports your next loan application. Visit 2ndstreetpropertymanagement.com to learn how professional property management translates directly into stronger financial reporting and better investment outcomes.

FAQ

What income counts as rental income for IRS purposes?

The IRS counts all payments you receive for the use of your property as rental income, including advance rent, security deposits kept as final rent, and services provided by tenants in lieu of rent. Report all of it on Schedule E.

Do I have to report rental income if I only rented for a few weeks?

If you rent your property for fewer than 15 days in a tax year, you do not report that income and cannot deduct rental expenses. Rent it for 15 days or more, and full reporting requirements apply.

How does depreciation work on a rental property?

The IRS requires straight-line depreciation of residential rental property over 27.5 years using MACRS GDS. Depreciation is mandatory; if you do not claim it, the IRS adjusts your cost basis as if you had, increasing your taxable gain at sale.

Can I deduct rental losses against my regular income?

Active participants with a modified AGI under $100,000 can deduct up to $25,000 in passive rental losses against ordinary income. That allowance phases out completely at $150,000 AGI.

What records do I need to keep for my rental property?

Keep signed leases, bank statements, receipts for all expenses, 1099 forms, and depreciation schedules. Retain records for at least three to six years, and keep cost basis records permanently.

Recommended

Comments