Rental Property Refinancing Explained for Investors

- Rey Rey Rodriguez

- 5 hours ago

- 8 min read

Rental property refinancing is the process of replacing your existing mortgage with a new loan to lower your interest rate, change your loan terms, or pull equity out of the property. Investors use three primary refinancing structures: rate-and-term refinances, cash-out refinances, and Debt Service Coverage Ratio (DSCR) loans. Each serves a different strategic purpose, and choosing the wrong one can cost you months of cash flow. This guide covers rental property refinancing explained from qualification to closing, so you can make decisions that actually move your portfolio forward.

What are the main types of rental property refinancing loans?

Rate-and-term refinancing replaces your current mortgage with a new one at a lower rate or different repayment schedule, without changing your loan balance. Cash-out refinancing increases your loan balance above what you currently owe, and you receive the difference as cash at closing. DSCR loans qualify you based on the property’s rental income rather than your personal income, making them a distinct category worth understanding separately.

Conventional vs. DSCR Refinance: Side-by-Side

Feature | Conventional Refinance | DSCR Refinance |

Income verification | Personal tax returns, W-2s | Rental income only |

Credit score minimum | Typically 620–680 | Typically 620–660 |

Max LTV (cash-out) | 75% | 70–75% |

Closing timeline | 30–45 days | 15–21 days |

Best for | W-2 or salaried investors | Self-employed, LLC holders |

Conventional loans require full personal income documentation, including two years of tax returns and bank statements. They suit investors with straightforward W-2 income and strong personal credit profiles. DSCR loans, by contrast, qualify on rental income alone, with ratio requirements ranging from 0.75x to 1.0x depending on the lender program.

Pro Tip: Compare APR across lenders, not just the base interest rate. Two loans with identical rates can carry very different total costs once origination fees and points are factored in.

Investment property loans carry a rate premium. Refinance rates run 0.25%–1.00% higher than comparable primary residence loans, reflecting the higher default risk lenders assign to non-owner-occupied properties. That spread matters when you are modeling cash flow projections over a 30-year hold.

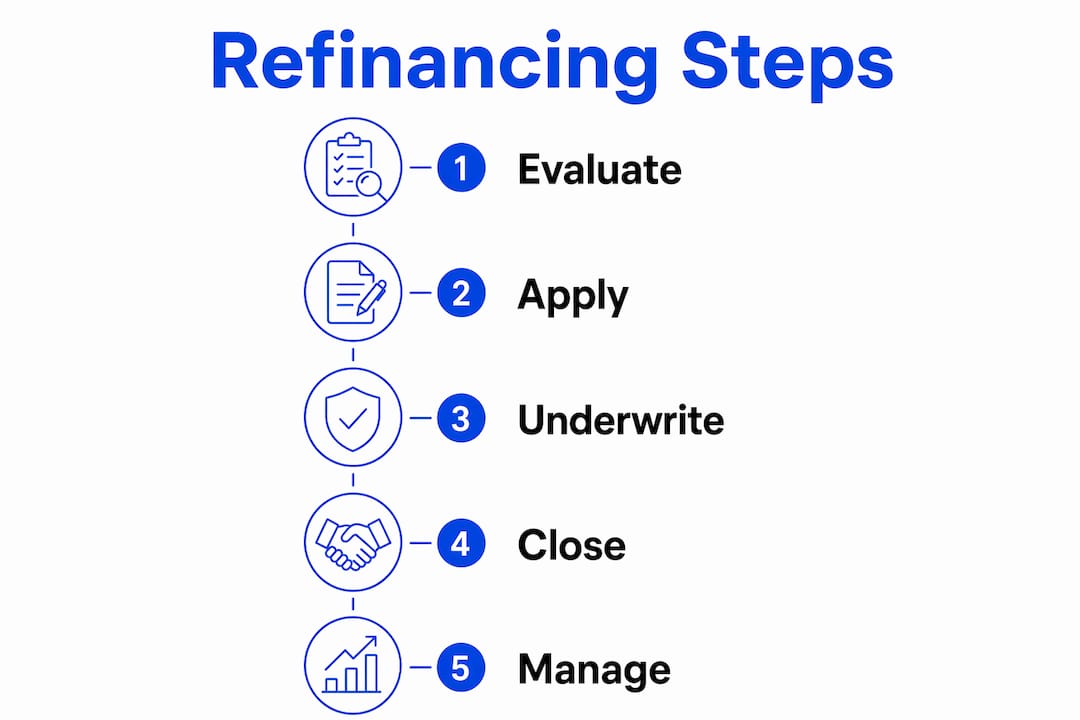

How does the rental property refinancing process work?

The refinance process follows a predictable sequence, but preparation separates investors who close in three weeks from those who drag through two months of back-and-forth with underwriters.

Define your goal. Decide whether you want a lower rate, a shorter term, or cash out. Your goal determines which loan product fits.

Pull your credit and review your equity position. Most lenders require a minimum 620 credit score for investment properties. Calculate your current LTV before applying.

Gather documentation. Conventional loans require two years of tax returns, recent bank statements, current leases, and a rent roll. DSCR loans need the lease agreement and a property appraisal.

Submit applications to multiple lenders. Rate shopping within a 14-day window counts as a single credit inquiry under FICO scoring models.

Lock your rate. Rate locks typically last 30–60 days. Locking too early or too late can increase your cost if rates shift during underwriting.

Complete the appraisal. The appraisal determines your LTV and directly controls how much cash you can pull out or what rate tier you qualify for.

Close and fund. Conventional loans close in 30–45 days. DSCR loans can close in as few as 15–21 days, which matters when you are trying to move quickly on an acquisition.

Closing costs run 2%–6% of the new loan amount. On a $300,000 refinance, that is $6,000–$18,000 out of pocket or rolled into the loan balance. Know this number before you sign anything.

Seasoning requirements add another timing variable. Most conventional lenders require 6–12 months of ownership before they will refinance. DSCR programs often allow refinancing after just six months, which is a real advantage for investors running a buy-and-hold acquisition strategy at pace.

Pro Tip: If your property is vacant at the time of refinancing, expect a 5% LTV reduction penalty from most lenders. Fill the unit before you apply whenever possible.

What are the benefits and risks of cash-out refinancing?

Cash-out refinancing is the most powerful tool in a rental investor’s financing toolkit, and also the most misused. The mechanics are straightforward: you refinance your property for more than you currently owe, and the lender cuts you a check for the difference at closing.

Most lenders cap cash-out refinances at 75% LTV on investment properties. If your property appraises at $400,000 and you owe $200,000, the maximum new loan is $300,000, giving you up to $100,000 in cash proceeds before closing costs.

Smart uses for cash-out proceeds:

Funding renovations that increase rental income or property value

Acquiring a second or third rental property as a down payment

Paying off higher-interest debt on another investment property

Building a cash reserve for capital expenditures across your portfolio

Pulling equity for personal expenses, vacations, or consumer debt is the fastest way to erode the compounding growth that makes rental property investing work. Treat cash-out proceeds as investment capital, not income.

The risk is real. A cash-out refinance increases your loan balance and your monthly payment. If your rental income does not cover the new debt service, you have traded long-term equity for short-term liquidity at a cost. Cash-out proceeds should fund investment-related uses that generate returns exceeding the cost of the new debt. That is the only math that makes sense.

For investors with rental property loan options across multiple properties, cash-out refinancing on a seasoned asset can fund the down payment on a new acquisition without touching personal savings. That is how experienced investors scale without waiting years to accumulate capital.

How do DSCR loans differ, and who should use them?

The Debt Service Coverage Ratio measures whether a property generates enough rental income to cover its mortgage payments. A DSCR of 1.25x means the property earns 25% more than its debt obligations. A DSCR of 1.0x means income exactly covers the payment.

DSCR loans are built around this single metric. Lenders evaluate the property’s cash flow, not your personal W-2 or tax returns. This structure creates significant advantages for a specific type of investor.

Investors who benefit most from DSCR loans:

Self-employed investors whose tax returns show low net income due to depreciation and deductions

Investors holding properties inside LLCs, where personal income separation complicates conventional underwriting

Investors with multiple financed properties who have hit conventional loan limits

Investors who want to close faster on refinances without assembling months of personal financial documentation

Some DSCR programs offer “no-ratio” options for strong borrowers, effectively removing the income validation hurdle entirely. These programs reflect how sophisticated the DSCR lending market has become for experienced investors.

The tradeoff is cost. DSCR loans typically carry slightly higher rates than conventional loans, and some programs require larger down payments or lower LTV caps on cash-out transactions. Use the DSCR calculator to model your property’s ratio before applying, so you know exactly where you stand before a lender pulls your credit.

Conventional underwriting counts every dollar of personal debt against you through the debt-to-income (DTI) ratio. DSCR underwriting ignores your personal DTI entirely. For investors with significant personal debt or complex income structures, that distinction is the difference between qualifying and not.

What strategic factors should you weigh before refinancing?

Refinancing a rental property without a clear purpose is the financial equivalent of confusing movement with progress. The decision should be driven by a specific investment objective, not by a rate drop alone.

Refinancing decisions should align with a strategy focused on deploying equity for higher-return uses, not chasing a quarter-point rate reduction that takes five years to break even on closing costs. Calculate your break-even point: divide total closing costs by your monthly savings. If you plan to sell before that date, the refinance costs you money.

Key factors to evaluate before you apply:

Equity deployment plan. Know exactly where cash-out proceeds will go and what return you expect from that deployment.

Vacancy status. A vacant property at closing triggers a 5% LTV penalty. Time your application around occupancy.

Seasoning timeline. Conventional lenders require 6–12 months of ownership. Plan acquisitions with this window in mind.

Rate lock timing. Rate locks last 30–60 days. Apply when you are ready to move, not when you are still deciding.

Total cost comparison. Compare APR and total fees, not just the interest rate, across at least three lenders.

Pro Tip: If you are refinancing to fund a new acquisition, coordinate your closing dates carefully. Cash-out proceeds from one property can fund the down payment on another, but the timing has to be deliberate.

Investors who finance rental properties with a long-term portfolio strategy in mind use refinancing as a tool for capital recycling, not a reaction to market rate movements. That mindset separates investors who build wealth from those who stay busy without building equity.

Key takeaways

Rental property refinancing builds wealth when equity is deployed into higher-return investments, not when it is extracted for personal use or chased for marginal rate savings.

Point | Details |

Know your loan type | Rate-and-term, cash-out, and DSCR loans serve different goals and require different qualification criteria. |

DSCR loans close faster | DSCR refinances close in 15–21 days versus 30–45 days for conventional loans, saving time on acquisitions. |

Cash-out LTV caps at 75% | Most lenders limit cash-out refinances to 75% LTV on investment properties, with a 5% penalty for vacant units. |

Seasoning affects timing | Conventional lenders require 6–12 months of ownership before refinancing; DSCR programs often allow six months. |

Compare APR, not just rate | Total loan cost includes origination fees and closing costs of 2%–6%, which must factor into your break-even analysis. |

What i have learned from watching investors refinance

The investors who get the most out of refinancing are the ones who treat it as a capital allocation decision, not a mortgage transaction. They come to the table knowing their DSCR, their target LTV, and exactly what they plan to do with any cash proceeds. The ones who struggle are usually chasing a rate they saw advertised without understanding the full cost structure.

The biggest mistake I see repeatedly is pulling cash out of a performing rental property to cover personal expenses or fund a lifestyle purchase. The math looks fine on the day of closing. Six months later, the higher monthly payment is compressing cash flow on a property that used to run smoothly. That investor just traded a productive asset’s equity for a depreciating personal expense.

DSCR loans changed the game for self-employed investors and LLC holders. Before these programs scaled, investors with complex tax returns were routinely denied conventional refinances despite owning profitable properties. Now, a property generating a 1.2x DSCR can qualify on its own merits. That is a structural shift in how investors can build and recycle capital.

One more thing: documentation preparation is the most underrated part of this process. Investors who have their rent rolls, leases, and bank statements organized before they apply move through underwriting in days, not weeks. Lenders reward preparedness with speed, and speed matters when you are trying to close on a new acquisition.

— Main

How 2ndstreetpropertymanagement supports your refinancing strategy

Refinancing a rental property is only as effective as the financial data behind the application. 2ndstreetpropertymanagement works with investors to keep rent rolls current, leases organized, and property financials in order so that when you are ready to refinance, your documentation is already lender-ready. That preparation directly shortens your underwriting timeline and strengthens your application. If you are building a portfolio and want a property management partner who understands the financing side of the business, explore our property management solutions built specifically for investors. We also recommend reviewing how to refinance for better rates as part of your lender comparison process.

FAQ

What is rental property refinancing?

Rental property refinancing is the process of replacing an existing mortgage on an investment property with a new loan to lower the interest rate, change the loan term, or access equity through a cash-out transaction.

How long does it take to refinance a rental property?

Conventional refinances close in 30–45 days, while DSCR loans can close in as few as 15–21 days, making DSCR the faster option for investors moving quickly on acquisitions.

What credit score do you need to refinance a rental property?

Most lenders require a minimum credit score of 620–680 for investment property refinances, with higher scores qualifying for better rates and higher LTV allowances.

What is a DSCR loan and who qualifies?

A DSCR loan qualifies borrowers based on the property’s rental income relative to its debt payments, with no personal tax returns or W-2s required, making it ideal for self-employed investors and LLC holders.

Is a cash-out refinance on a rental property worth it?

A cash-out refinance is worth it when the proceeds are deployed into investments that generate returns exceeding the new loan’s cost. Pulling equity for personal expenses erodes portfolio growth and compresses monthly cash flow.

Recommended

Comments