Rental Property Portfolio Explained for Investors

- Rey Rey Rodriguez

- 3 hours ago

- 8 min read

A rental property portfolio is a strategic collection of rental properties held together to generate income and capital growth. Understanding how to build rental property portfolio structures, finance them correctly, and track the right metrics separates investors who scale from those who stall. This article breaks down the rental property portfolio explained from every angle: portfolio landlord thresholds, portfolio loans, key financial metrics like DSCR and operating expense ratios, and the management practices that keep growth sustainable.

What is a rental property portfolio, really?

A rental property portfolio is an investor’s collection of rental properties managed under a unified strategy for income and capital growth. Owning two single-family homes is a start. Owning ten properties across multiple markets, financed strategically and tracked through a single dashboard, is a portfolio. The distinction matters because the tools, financing structures, and performance metrics change significantly as you cross certain thresholds.

Defining your investment purpose before buying your second or third property is the single most important decision you will make. Income-first investors prioritize cash flow and choose high-yield markets. Growth-first investors accept thinner margins in appreciation-heavy markets. A balanced approach splits the difference. Your purpose drives location selection, property type, financing structure, and exit planning. Without it, you confuse movement with progress.

How does financing change when you become a portfolio landlord?

A portfolio landlord is defined as an investor with four or more mortgaged buy-to-let properties. That threshold is not arbitrary. Under PRA guidelines since 2017, lenders are required to apply portfolio-level underwriting to any mortgage application or refinance from an investor at or above that threshold. This changes everything about how you apply for financing.

Single-property underwriting looks at one asset in isolation: its rental income, its value, and your personal income. Portfolio underwriting looks at the whole picture. Lenders assess your aggregate rental income, total mortgage debt across all properties, and apply stress tests to your entire portfolio cash flow. A property that would qualify easily on its own may face scrutiny if it weakens your overall numbers.

Here is what lenders typically request at the portfolio level:

A full property schedule listing every address, current value, outstanding mortgage balance, monthly rental income, and remaining loan term

Stressed interest coverage ratios applied across the whole portfolio

Loan-to-value ratios calculated on aggregate portfolio value

Evidence of rental income through tenancy agreements or rental history

Pro Tip: Maintain a live property schedule in a spreadsheet before you hit four properties. Lenders will request this document, and having it ready signals professionalism and speeds up the underwriting process considerably.

The administrative burden of portfolio-level underwriting catches many investors off guard. Preparing for it early is not optional. It is the price of scaling.

How do rental portfolio loans work?

A rental portfolio loan bundles multiple properties into a single mortgage, replacing several individual loans with one closing, one lender relationship, and one monthly payment. Portfolio loans can save roughly $8,000–$12,000 compared to closing five individual loans separately. That savings comes from reduced closing costs, fewer title searches, and consolidated underwriting fees.

The underwriting model for portfolio loans is built around blended DSCR. Rather than requiring every property to meet a minimum Debt Service Coverage Ratio independently, the lender calculates a single DSCR across all bundled assets. This means stronger properties offset weaker ones by blending their cash flows. A high-performing duplex can carry a recently vacated single-family home through a rough quarter without triggering a default concern.

Feature | Individual Loans | Portfolio Loan |

Closings required | One per property | Single closing |

Underwriting basis | Per-property DSCR | Blended portfolio DSCR |

Estimated cost savings | Baseline | $8,000–$12,000 |

Lender relationships | Multiple | One |

Flexibility | Higher per asset | Tied to portfolio performance |

Typical qualification criteria for portfolio loans include a minimum credit score around 680, loan-to-value ratios at or below 75–80%, and a blended DSCR above 1.20. Amortization periods commonly run 20–30 years, with some lenders offering interest-only periods for the first few years.

Pro Tip: Use a DSCR calculator to model your blended ratio before approaching portfolio lenders. Knowing your number in advance lets you negotiate from a position of strength rather than reacting to lender feedback.

What financial metrics should every portfolio investor track?

Rental property cash flow explained at the portfolio level requires three core metrics: DSCR, Operating Expense Ratio, and carrying costs. Each one tells a different part of the story.

Debt service coverage ratio (DSCR)

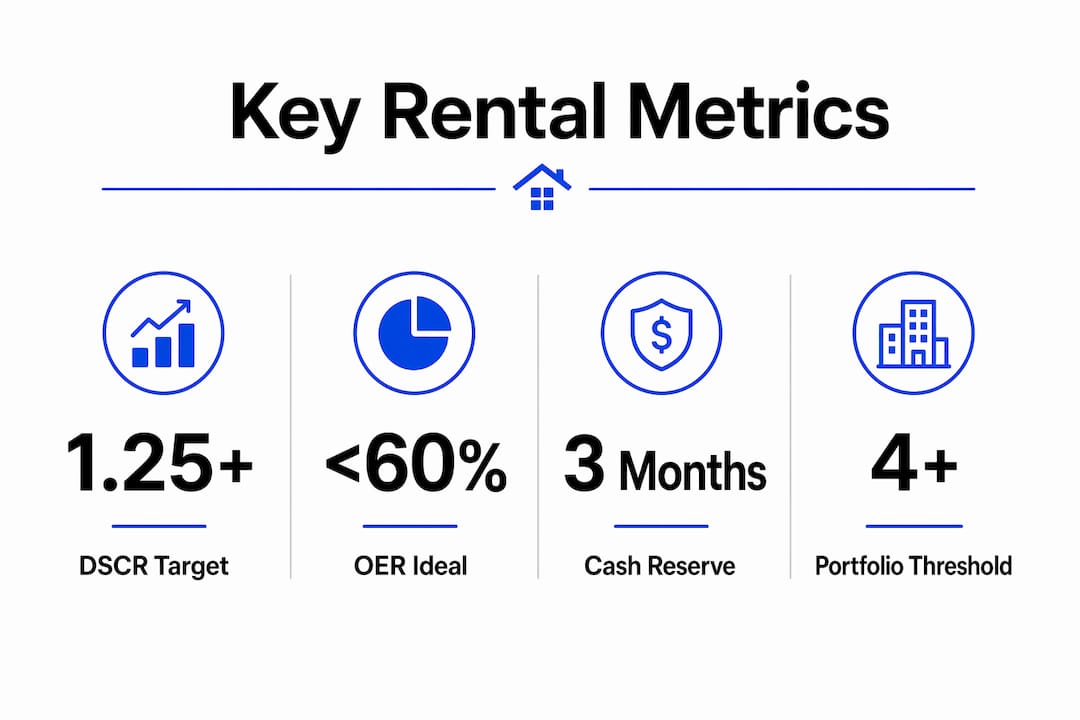

DSCR is calculated as Net Operating Income divided by annual debt service. A DSCR of 1.25 means your NOI covers your debt payments with a 25% cushion. A DSCR below 1.0 means your properties are not generating enough income to cover their own debt. Most lenders require a minimum DSCR of 1.20–1.25 for portfolio loans. Improving your DSCR means either increasing NOI through rent increases and expense cuts or reducing debt service through refinancing.

Operating expense ratio (OER)

The Operating Expense Ratio is total operating expenses divided by gross operating income. Residential benchmarks fall between 60% and 80%, meaning for every dollar of gross income, 60–80 cents covers operating costs. A rising OER signals cost drift or inefficiency. Tracking OER trends over time reveals whether your portfolio is becoming more or less efficient. An OER creeping above 80% is a warning sign that demands investigation before it becomes a cash flow problem.

Carrying costs and vacancy impact

Carrying costs include mortgage payments, property taxes, insurance, and utilities that continue even when a unit sits vacant. A single vacancy month on a property with $2,000 in monthly carrying costs wipes out two to three months of expected positive cash flow. Model your break-even occupancy rate for every property. If a property needs 85% occupancy to cover its carrying costs and your market averages 78%, you have a structural cash flow problem, not a temporary one.

The table below summarizes the three metrics and their practical thresholds:

Metric | Formula | Target Threshold |

DSCR | NOI / Annual Debt Service | Above 1.25 |

Operating Expense Ratio | Total Operating Expenses / Gross Operating Income | Below 75% |

Break-Even Occupancy | Carrying Costs / Gross Potential Rent | Below market vacancy rate |

How do you manage and scale a rental portfolio sustainably?

Scaling a rental portfolio without a system is how investors end up with ten properties and zero clarity. The solution is treating your portfolio like a business with defined processes, not a collection of individual transactions.

Set a clear investment purpose first. Income-first, growth-first, or balanced strategies require different property types, markets, and financing structures. Decide before you buy, not after.

Diversify by location and tenant type. Concentrating all properties in one zip code or one tenant demographic creates correlated risk. A local economic downturn hits every property simultaneously. Spread across two or three markets to reduce that exposure.

Build a portfolio dashboard. A rental property dashboard tracks total properties, rental income, operating expenses, occupancy rates, and vacancy trends in one view. Dashboards that segment KPIs by location and property type identify underperforming assets before they become liabilities.

Refinance equity strategically. As properties appreciate, refinancing releases equity for new acquisitions without requiring out-of-pocket capital. This is the primary engine of portfolio growth for most experienced investors.

Consolidate financing when it makes sense. Portfolio loan consolidation reduces the administrative burden of managing multiple lender relationships, multiple payment schedules, and multiple renewal dates. Fewer moving parts mean fewer opportunities for error.

Pro Tip: Maintain a cash reserve equal to three months of carrying costs across your entire portfolio. This buffer absorbs vacancy, unexpected repairs, and interest rate adjustments without forcing you into reactive decisions.

For deeper guidance on building from scratch, the process of identifying your first few properties and structuring them for long-term growth deserves its own focused attention.

Key takeaways

A rental property portfolio requires portfolio-level financing, disciplined metric tracking, and a clear investment purpose to generate sustainable long-term returns.

Point | Details |

Portfolio landlord threshold | Four or more mortgaged properties triggers portfolio-level underwriting under PRA guidelines. |

Portfolio loans save money | Bundling properties into one loan saves roughly $8,000–$12,000 versus five individual closings. |

DSCR is the core metric | A DSCR above 1.25 signals your NOI covers debt with a meaningful safety cushion. |

OER reveals efficiency trends | Residential OER benchmarks fall between 60% and 80%; anything rising above 80% demands review. |

Carrying costs require buffers | Vacancy months eliminate multiple months of positive cash flow without a reserve in place. |

What i’ve learned after years of watching portfolios succeed and fail

The investors who build durable portfolios share one trait: they define their purpose before they define their target. Every decision flows from that anchor. The ones who struggle are usually chasing deals without a framework. They buy in three different states, with three different financing structures, tracking nothing in a spreadsheet they update twice a year. That is not a portfolio. That is a collection of problems waiting to compound.

The metric I see ignored most often is the Operating Expense Ratio. Investors obsess over gross rent and purchase price, but OER tells you whether the asset is actually efficient to operate. A property with strong rent but a rising OER is quietly eroding your returns. Catching that trend early, before it becomes a structural problem, is what separates disciplined portfolio management from wishful thinking.

The other lesson is about financing consolidation. Most investors wait too long to explore portfolio loans. They manage five lenders, five renewal dates, and five sets of covenants, and wonder why scaling feels exhausting. Consolidating into a single portfolio loan does not just save money at closing. It frees up mental bandwidth that you can redirect toward finding the next acquisition.

Scaling beyond ten doors is absolutely achievable. But it requires systems, buffers, and a willingness to treat your portfolio as a business. The investors who do that consistently are the ones still growing at twenty doors, thirty doors, and beyond.

— Main

How 2ndstreetpropertymanagement helps you scale with confidence

Managing a growing rental portfolio demands more than spreadsheets and good intentions. 2ndstreetpropertymanagement is built by investors for investors, which means the team understands portfolio-level challenges from the inside.

From tracking occupancy and expenses across multiple properties to coordinating maintenance and tenant relationships at scale, 2ndstreetpropertymanagement handles the operational complexity so you can focus on growth. Whether you are managing your first four properties or your fortieth, professional portfolio management support gives you the clarity and capacity to make better decisions faster. Explore how 2ndstreetpropertymanagement can take the operational weight off your plate and keep your portfolio performing.

FAQ

What is a rental property portfolio?

A rental property portfolio is a collection of rental properties held by one investor under a unified strategy for generating income and capital growth. Portfolios are managed as a single financial unit rather than as separate, unrelated assets.

When does a landlord become a portfolio landlord?

An investor becomes a portfolio landlord at four or more mortgaged buy-to-let properties. This threshold triggers portfolio-level underwriting requirements under PRA guidelines, requiring lenders to assess aggregate income and debt across all properties.

What is DSCR and why does it matter for rental portfolios?

DSCR is Net Operating Income divided by annual debt service. Lenders require a minimum DSCR of 1.20–1.25 for portfolio loans, meaning your rental income must cover debt payments with a meaningful buffer above 1.0.

How do carrying costs affect rental property cash flow?

Carrying costs are fixed expenses like mortgage payments, taxes, and insurance that continue during vacancy. A single vacant month can eliminate several months of positive cash flow, making cash reserves and break-even occupancy modeling critical for portfolio health.

What is a good operating expense ratio for rental properties?

A good Operating Expense Ratio for residential rental properties falls between 60% and 80%. An OER trending above 80% signals rising inefficiency or cost drift and requires immediate review of operating expenses.

Recommended

Rental Portfolio Strategies: Building a Successful Rental Property Portfolio

Rental Property Portfolio Tips: Building Your Rental Property Portfolio the Smart Way

Rental Portfolio Development Tips: Building a Robust Rental Property Portfolio

Rental Portfolio Building Tips: Building a Successful Rental Portfolio from Scratch

Comments