Investing for Beginners: Build Wealth Starting Today

- Rey Rey Rodriguez

- Jul 2

- 7 min read

Investing is defined as putting money to work in assets that grow in value over time, building wealth beyond what a savings account can deliver. For a beginner investor, the goal is not to pick the next hot stock. The goal is to build a disciplined habit of consistent contributions tied to clear financial goals. Starting with manageable amounts and the right account types gives you a real edge over those who wait for perfect conditions. This guide covers the fundamentals of investing for beginners, from strategy and account selection to your first practical steps.

What are the best beginner investment strategies?

Dollar-cost averaging is the single most effective strategy for new investors. It means investing a fixed dollar amount at regular intervals, regardless of whether the market is up or down. Dollar-cost averaging removes emotional decisions and eliminates the temptation to time the market. Over time, you buy more shares when prices are low and fewer when prices are high, which lowers your average cost per share.

Diversification is the second pillar of sound beginner investment strategies. Spreading your money across many assets reduces the damage any single loss can do to your portfolio. Low-cost index funds and ETFs (exchange-traded funds) are the most practical tools for this. A single S&P 500 index fund gives you exposure to 500 of the largest American companies in one purchase.

The biggest mistake most beginner investors make is focusing on specific stocks rather than on their overall goals and risk tolerance. Chasing individual stocks confuses movement with progress. A diversified index fund portfolio aligned with your timeline beats stock-picking for the vast majority of new investors.

Robo-advisors are a third option worth knowing. These are automated platforms that build and manage a diversified portfolio for you based on your risk tolerance and goals. Robo-advisors charge annual fees of 0.25% to 0.50%, plus fund expense ratios. That fee is reasonable for a hands-off, fully managed portfolio, but you should understand what you are paying before you sign up.

Dollar-cost averaging: Invest a fixed amount on a set schedule, weekly or monthly, regardless of market conditions.

Index funds and ETFs: Buy broad-market funds that track the S&P 500 or total market to diversify instantly.

Robo-advisors: Use automated platforms for a managed, diversified portfolio with minimal effort.

Risk and time horizon alignment: Stocks suit long-term goals (10+ years); cash alternatives and bonds suit shorter timelines.

Avoid market timing: No one consistently predicts market highs and lows. Consistency beats prediction every time.

Pro Tip: Set up automatic monthly contributions the day after your paycheck clears. Automating removes the decision entirely and keeps you consistent through every market cycle.

How much money do you really need to start investing?

The barrier to entry for investing is lower than most beginners expect. Most major brokerage firms now offer $0 account minimums and zero-commission trading. You can open an account today with no money and fund it when you are ready.

Fractional shares allow you to invest in expensive stocks or ETFs for as little as $1 to $5. That means you can own a piece of a high-priced index fund without needing hundreds of dollars upfront. Starting with $50 to $100 per month builds the habit and lets compounding begin working in your favor.

The power of compounding is not theoretical. Investing $250 monthly over 40 years in the S&P 500 can grow to approximately $1.8 million, with only $120,000 actually contributed. The rest is compounding at work. Starting early matters far more than starting with a large amount.

Account type | Tax treatment | Best for |

Taxable brokerage | No tax advantage; capital gains taxed | Flexible goals, no contribution limits |

Traditional 401(k) | Pre-tax contributions; taxed on withdrawal | Employer-sponsored retirement savings |

Roth IRA | After-tax contributions; tax-free growth | Long-term retirement with tax-free withdrawals |

Traditional IRA | Pre-tax or after-tax; taxed on withdrawal | Retirement savings without employer plan |

Pro Tip: If your employer offers a 401(k) match, contribute at least enough to capture the full match before investing anywhere else. A 100% immediate return on your contribution is the best guaranteed return available to any investor.

Which investment accounts should beginners consider?

Choosing the right account type is as important as choosing what to invest in. Tax-advantaged accounts like 401(k)s and IRAs let your money grow without annual tax drag, which compounds significantly over decades. Taxable brokerage accounts offer flexibility with no contribution limits but no tax shelter.

A 401(k) through your employer is the first account most beginners should fund, especially when a match is available. After capturing the full employer match, a Roth IRA is the next priority for most beginners. Roth IRA contributions grow tax-free, and qualified withdrawals in retirement are also tax-free. The IRS sets annual contribution limits for both account types, so check current limits each year.

Target-date funds are worth knowing about. These are single funds that automatically shift from aggressive (more stocks) to conservative (more bonds) as your target retirement year approaches. They are built for beginners who want a complete, self-managing portfolio in one fund. Many 401(k) plans offer target-date funds as a default option.

401(k): Funded with pre-tax dollars; reduces taxable income now; ideal first account when an employer match exists.

Roth IRA: Funded with after-tax dollars; tax-free growth and withdrawals; best for investors expecting higher income in retirement.

Traditional IRA: Pre-tax or after-tax depending on income; good supplement when 401(k) limits are reached.

Taxable brokerage: No contribution limits; full flexibility; best for goals outside retirement or after maxing tax-advantaged accounts.

Target-date funds: Single-fund solution that rebalances automatically; ideal for beginners who want simplicity.

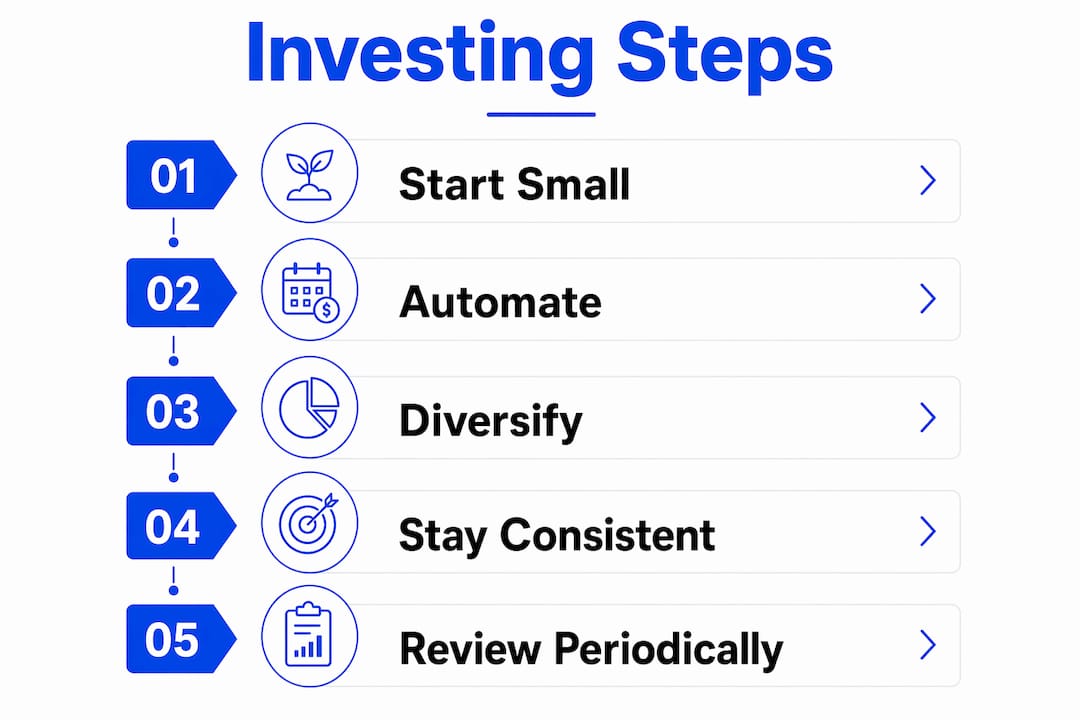

What practical first steps should a novice investor take?

A clear action plan removes the paralysis that stops most beginners from starting. Follow these steps in order and you will have a functioning investment portfolio within a week.

Set a specific financial goal. Define what you are investing for, retirement, a down payment, or financial independence, and attach a timeline to it. Goals drive every decision that follows, from account type to asset allocation.

Build a small emergency fund first. Three months of expenses in a high-yield savings account protects your investments from being liquidated during a personal financial crisis. This is not optional; it is the foundation.

Choose a brokerage with low fees and a clean interface. Look for $0 commissions, no account minimums, and fractional share availability. Beginners are recommended to invest about 10% to 15% of income, so pick a platform that makes recurring contributions easy.

Open the right account for your goal. Use a 401(k) for employer-matched retirement savings. Use a Roth IRA for long-term tax-free growth. Use a taxable brokerage for flexible, non-retirement goals.

Start with a low-cost index fund or ETF. A total market index fund or S&P 500 ETF gives you instant diversification at minimal cost. Expense ratios below 0.10% are standard for major index funds today.

Automate your contributions. Set a recurring transfer from your checking account to your investment account on a fixed date each month. Automation is the single most reliable way to stay consistent.

Review your portfolio quarterly, not daily. Checking your balance every day creates anxiety and encourages bad decisions. Quarterly reviews keep you informed without triggering emotional reactions to short-term volatility.

Real estate is another path worth exploring alongside traditional investing. If you want to understand how property fits into a long-term wealth plan, the guide on real estate investment fundamentals breaks down the basics clearly.

Key takeaways

Starting early with consistent, automated contributions is the single most powerful move a beginner investor can make, regardless of the amount.

Point | Details |

Start small, start now | Most brokerages require $0 to open an account; fractional shares let you begin with $1 to $5. |

Use dollar-cost averaging | Invest a fixed amount on a set schedule to remove emotion and build long-term discipline. |

Capture the employer match first | A 401(k) match delivers an immediate 100% return; always contribute enough to claim it fully. |

Choose the right account type | Tax-advantaged accounts (401(k), Roth IRA) grow faster than taxable accounts over decades. |

Diversify with index funds | A single S&P 500 or total market index fund provides broad diversification at minimal cost. |

Why waiting for the “right time” is the costliest mistake

The most common thing I hear from new investors is some version of “I’ll start when I have more money” or “I’ll wait until the market settles down.” I understand the hesitation. The market feels unpredictable, and the fear of losing money is real. But waiting is not a neutral decision. Every month you delay is a month compounding does not work for you.

The math is unforgiving in that regard. A 25-year-old who invests $200 per month will end up with significantly more than a 35-year-old investing the same amount, even though the 35-year-old contributes for just as long. Time in the market beats timing the market, every single time.

What I have also seen is that beginners who wait for perfect conditions never find them. There is always a reason to delay: inflation, election uncertainty, interest rate changes. The investors who build real wealth are not the ones who found the perfect entry point. They are the ones who started with what they had, stayed consistent, and let time do the heavy lifting.

You do not need to understand every financial concept before you start. You need a goal, a basic account, and a low-cost index fund. Learn as you go. The strategies that build wealth through real estate follow the same principle: start with fundamentals, stay disciplined, and let time compound your results.

— Main

How 2ndstreetpropertymanagement supports new investors

Building wealth through investing takes more than picking the right fund. It takes a clear strategy, the right assets, and guidance from people who have done it themselves.

2ndstreetpropertymanagement is built by investors, for investors. Whether you are just starting with traditional accounts or ready to explore real estate as part of your portfolio, the team at 2ndstreetpropertymanagement brings hands-on experience to every conversation. Real estate investing offers cash flow, appreciation, debt paydown, and depreciation benefits that stock portfolios cannot replicate. If you want to see how property fits into a long-term investment plan, 2ndstreetpropertymanagement is the place to start.

FAQ

What is the best investment for a beginner?

Low-cost index funds tracking the S&P 500 or total market are the best starting point for most beginners. They provide instant diversification, low expense ratios, and consistent long-term performance without requiring active management.

How much should a beginner invest each month?

Beginners are recommended to invest 10% to 15% of their income. Starting with $50 to $100 per month is effective if that is what your budget allows; consistency matters more than the amount.

What is dollar-cost averaging?

Dollar-cost averaging means investing a fixed dollar amount at regular intervals regardless of market conditions. It reduces the impact of volatility and removes the temptation to time the market.

Should a beginner use a robo-advisor?

Robo-advisors are a practical option for beginners who want a managed, diversified portfolio without making individual investment decisions. They charge annual fees of 0.25% to 0.50%, which is reasonable for the service provided.

Is real estate a good investment for beginners?

Real estate can be an excellent complement to traditional investing, offering cash flow, appreciation, and tax advantages. Beginners should understand the basics of real estate investing before committing capital to property.

Recommended

Comments