Rental Property LLC Structure Explained for Investors

- Rey Rey Rodriguez

- 2 days ago

- 9 min read

Most investors forming an LLC for their rental properties assume two things: that their personal assets are now completely protected and that their taxes just got simpler. Both assumptions are partially wrong. The rental property LLC structure explained in this guide covers the legal mechanics, the different structural options, the real tax implications, and the setup process in enough detail to help you make a decision that fits your actual portfolio. Whether you own one rental or ten, the structure you choose matters more than the fact that you chose an LLC at all.

Table of Contents

Key takeaways

Point | Details |

LLC is not automatic protection | Liability only holds if you maintain strict separation between personal and business finances. |

Structure choice depends on portfolio size | Single LLCs suit smaller portfolios; separate or series LLCs work better as value and risk increase. |

Pass-through taxation is standard | Rental income flows to your personal return, but multi-member LLCs add filing complexity. |

Deed transfer is non-negotiable | Without recording the property in the LLC’s name, the liability shield does not apply. |

Ongoing compliance is required | Annual state filings, separate accounts, and updated insurance keep the LLC valid and effective. |

Rental property LLC structure explained

An LLC, or Limited Liability Company, is a legal entity that separates your investment assets from your personal ones. When you hold a rental property inside an LLC, a lawsuit from a tenant or contractor targets the LLC’s assets, not your savings account, your primary home, or your other investments. That separation is the core value proposition.

Here is how it works in practice. You form the LLC with your state, transfer the property deed into the LLC’s name, open a dedicated business bank account, and run all income and expenses through that account. The LLC becomes the landlord of record. You are a member of the LLC, not the personal owner of the property.

A few structural fundamentals matter from day one:

Operating agreement: This document defines ownership percentages, decision-making authority, and what happens if a member exits. Without one, your state’s default LLC rules apply, which may not reflect your intentions.

Registered agent: Every LLC needs a registered agent, a person or service that receives legal documents on the LLC’s behalf. This can be you or a paid service.

Corporate formalities: Unlike a corporation, an LLC has fewer formalities, but you still need to keep records, hold documented decisions, and file annual reports in most states.

Pass-through taxation: The LLC itself does not pay federal income tax. Profits and losses pass through to your personal return, which is reported on Schedule E for single-member LLCs.

The 21.6 million active LLCs operating in 2025 reflect how widely investors have adopted this structure. But sheer popularity does not mean it is always the right call or that it works automatically without proper maintenance.

Pro Tip: Open the LLC’s bank account before the first rent payment arrives. Even one deposit into your personal account blurs the financial separation that makes the LLC legally meaningful.

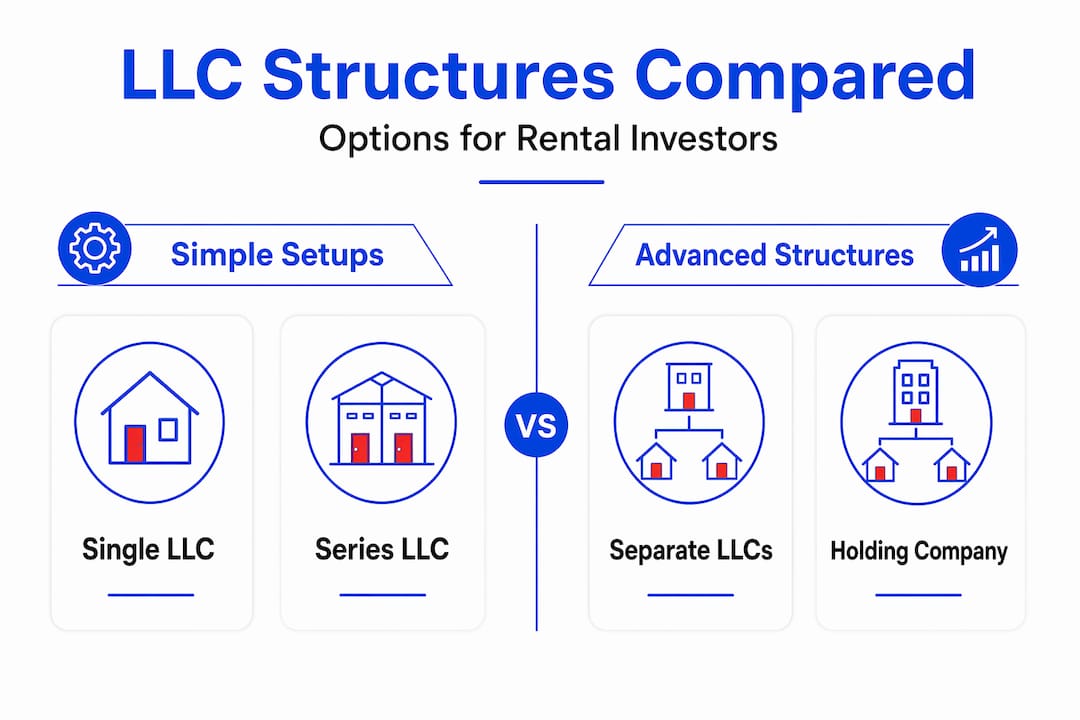

Comparing LLC structures for rental portfolios

Not every LLC setup is the same, and the difference between a $90,000 asset and a $600,000 asset should influence which structure you use. Here is a breakdown of the four most common approaches.

Structure | Best for | Asset protection | Estimated cost | Complexity |

Single LLC (all properties) | 1 to 5 lower-value rentals | Moderate | Low | Low |

Separate LLC per property | High-value or high-risk properties | Maximum | High | High |

Series LLC | Mid-size portfolios in eligible states | Moderate to high | Medium | Medium |

Holding company with subsidiaries | Large portfolios (5+ properties) | High | High | High |

Single LLC for all properties is the most common starting point. It is simple to manage and costs less to maintain. The problem is shared risk. One lawsuit tied to one property can potentially reach all the assets held inside that same LLC. A single LLC works well for portfolios of 1 to 5 properties, but for higher-value assets, that shared exposure becomes a real vulnerability.

Separate LLCs per property give you maximum isolation. A claim against one property stays walled off from the others. The trade-off is cost and paperwork. Each LLC requires its own formation fees, registered agent, bank account, and annual state filing. This is the preferred approach for high-value properties above $500K or any property that carries elevated liability risk, such as a short-term rental or a property with a pool.

Series LLCs offer a middle-ground solution. A single parent LLC contains separate “series,” each of which holds its own property and has its own liability shield. Series LLCs are permitted in roughly 20 states, including Texas and Delaware. The appeal is real: you get isolation without forming a completely separate entity for every property. The concern is that court precedents on series LLCs remain limited, and some lenders are hesitant to work with them.

Holding company structures are built for larger portfolios. A parent LLC owns subsidiary LLCs, each holding one or a group of properties. This model allows holding companies to streamline management across a large portfolio while maintaining liability separation between subsidiaries. The administrative overhead is significant, but so is the protection when you are managing millions in real estate.

For your real estate investment planning, matching your LLC structure to your portfolio size and risk profile is as important as choosing the right property in the first place.

How to set up and maintain a rental property LLC

Setting up an LLC for rental properties is straightforward when you follow the steps in order. Skipping or rushing any step creates gaps that can undermine the entire structure later.

Choose your LLC structure. Based on your portfolio size, property values, and state availability, decide whether a single LLC, separate LLCs, or a series LLC makes sense.

Select and register your LLC name. Your state’s business portal will let you search for name availability. Choose something clear and professional, and avoid using your personal name directly to reinforce the separation.

File Articles of Organization. This is the official formation document filed with your state. Texas LLC formation fees run around $300, and most states charge somewhere in that range.

Obtain an EIN. An Employer Identification Number from the IRS is required to open a business bank account and file taxes. You can get one online in minutes at no cost.

Draft an operating agreement. Even if your state does not require one, this document protects you. It defines ownership shares, profit distributions, and decision-making rules.

Open a separate business bank account. Every dollar of rent goes in here. Every expense comes out of here. No exceptions.

Transfer the property deed. Without recording the deed in the LLC’s name with the county clerk, the liability shield does not apply. This step is where many investors stall out, and it is the most consequential one.

Update your insurance. Your existing landlord policy may not cover claims when the property is titled to an LLC. Insurance policies often require updating to name the LLC as the insured party.

Monitor ongoing compliance. Most states require annual reports and fees to keep the LLC active. Missing these can result in administrative dissolution, which voids your protection retroactively.

Pro Tip: Check whether your existing mortgage has a due-on-sale clause before transferring the deed. Lenders often do not enforce this clause for owner transfers to their own LLC, but it is worth a conversation with your lender before you file anything.

Tax implications of rental property LLCs

The tax structure of a rental property LLC is one of its most misunderstood features. Let’s clarify what actually changes when your rental is held inside an LLC.

For a single-member LLC, nothing changes on the tax side at the federal level. The IRS treats a single-member LLC as a disregarded entity, which means rental income and expenses still flow to Schedule E on your personal return. You do not file a separate federal return for the LLC.

For a multi-member LLC, the IRS treats it as a partnership. That means filing a Form 1065 partnership return each year, then issuing K-1 forms to each member showing their share of income and losses. Adding co-ownership through an LLC shifts the filing requirement from a simple Schedule E to a more complex partnership return, which adds both time and cost.

The deductions available to LLC-owned rentals are the same as those for personally owned rentals: mortgage interest, property taxes, depreciation, repairs, insurance, and management fees. For a deeper look at how cash flow and taxable income diverge for rental investors, the breakdown of rental property tax mechanics at 2ndstreetpropertymanagement.com is worth reading before your next filing.

A few specific tax considerations to keep in mind:

Qualified Business Income deduction: Some rental property owners may qualify for the 20% QBI deduction under Section 199A, but it requires meeting certain income and activity thresholds. Consult a CPA before assuming you qualify.

Financing friction: Holding property in an LLC complicates financing because residential loan programs generally favor individual borrowers. Expect higher rates or commercial loan terms for LLC-held properties.

Pass-through taxation avoids double taxation, which is a real advantage over C-corporations for rental investors, but it does not reduce your tax bill automatically. The structure just determines where the income lands.

Understanding these distinctions early saves expensive corrections later. Real tax advantages of real estate come from depreciation and deductions, not from the LLC wrapper itself.

Common pitfalls and how to avoid them

The LLC structure works until it does not. Most of the time it fails because of investor behavior, not legal loopholes.

“Forming an LLC is step one. Maintaining it correctly is the actual job. Skipping the small stuff is how you lose the big protection.”

The most common mistakes worth knowing:

Commingling funds. Using your LLC account to pay a personal bill, even once, gives opposing attorneys an opening to argue the LLC is not a real separate entity. Maintaining separate accounts and records is the single most effective way to protect the veil.

Skipping the deed transfer. The LLC is meaningless as a shield if the property title still shows your personal name. Recording the deed with the county clerk is not optional.

Assuming full immunity. Personal negligence can pierce LLC protection. If you personally made a negligent decision that caused harm, the LLC structure may not protect you from personal liability in that specific scenario.

Neglecting insurance coordination. Your landlord policy and your LLC structure must align. A policy that names you personally on a property titled to an LLC may result in a denied claim.

Pro Tip: Review your operating agreement and LLC records annually, not just at formation. Courts look at whether you treated the LLC as a real business over time, not just on the day you filed.

My take on LLC structuring for rental investors

I’ve seen investors spend thousands on multi-LLC setups for portfolios that genuinely did not need them. And I’ve seen others try to protect a $700,000 property inside a single LLC they shared with four other low-value rentals, which was the equivalent of keeping all your valuables in one unlocked box.

The honest truth is that most investors underestimate what it costs to maintain multiple LLCs correctly. Formation fees are just the beginning. Add registered agent costs, annual state filings, separate bookkeeping, and a CPA who understands entity-level reporting, and the annual overhead per LLC often runs $500 to $1,500 or more.

My personal framework: one or two lower-value rentals can comfortably sit in a single LLC if you maintain clean books and keep the operating agreement tight. High-value properties deserve their own entity, full stop. For a growing mid-size portfolio, a series LLC in a state that supports them is worth exploring, but get a real estate attorney who has actually worked with them, not just one who has read about them.

The no one-size-fits-all reality of LLC structuring is why cookie-cutter advice fails investors. Your structure should reflect your portfolio’s risk profile, your state’s laws, and your capacity for ongoing administration.

Do not skip the professionals. A real estate attorney handles the deed transfer and operating agreement. A CPA handles the tax elections and filing strategy. The upfront cost of getting both right is a fraction of what you pay to unwind a bad structure later.

— Main

How 2ndstreetpropertymanagement helps LLC investors

Managing rental properties through an LLC adds a layer of financial and administrative responsibility that grows with every property you add to your portfolio.

2ndstreetpropertymanagement was built by investors who understand what that complexity actually looks like in practice. From keeping income and expense records that hold up under scrutiny to coordinating with your legal and tax team on LLC compliance requirements, professional property management protects the structure you worked to build. When your properties are managed with the same rigor your LLC demands, cash flow stays clean and your liability shield stays intact. Explore how our property management services support LLC-structured rental portfolios, and see why investors trust us to protect both their properties and their bottom line.

FAQ

What is a rental property LLC structure?

A rental property LLC structure is a legal arrangement where one or more investment properties are held inside a Limited Liability Company, separating the investor’s personal assets from business liabilities and enabling pass-through taxation.

Does an LLC eliminate all personal liability for landlords?

No. An LLC limits liability but does not eliminate it entirely. Personal negligence, fraud, or commingling funds can allow courts to pierce the LLC’s protection and hold you personally responsible.

How many LLCs do I need for my rental properties?

It depends on your portfolio size and risk level. One LLC works for small portfolios of lower-value rentals, while high-value or high-risk properties generally warrant their own separate LLC for maximum protection.

Does transferring property to an LLC trigger the due-on-sale clause?

Technically yes, but lenders often do not enforce this clause when an owner transfers a property to their own LLC. Confirm with your lender before making the transfer to avoid surprises.

How does LLC ownership affect my rental property taxes?

A single-member LLC is taxed as a disregarded entity, so rental income still flows to Schedule E on your personal return. A multi-member LLC files a partnership return, which adds reporting complexity and cost.

Recommended

Comments