Rental Property Asset Protection Explained for Landlords

- Rey Rey Rodriguez

- 1 hour ago

- 9 min read

Most landlords think they’re covered. They have a homeowner’s policy, maybe an LLC, and call it done. That assumption is exactly what makes rental property asset protection explained so poorly in practice. A single slip-and-fall lawsuit can pierce through a poorly maintained LLC, exhaust your insurance limits, and reach your personal savings. Your entire portfolio can be at risk from one bad tenant, one negligent contractor, or one missed formality. The good news is that a layered, coordinated protection system can stop that from happening. Here is how to build one.

Table of Contents

Key takeaways

Point | Details |

Insurance is your first line | Landlord insurance and umbrella policies cover what standard homeowner policies miss, including lost rental income. |

LLCs require active maintenance | A neglected LLC can be pierced by courts, exposing personal assets to liability claims. |

Equity positioning deters creditors | Lowering exposed equity through mortgages and liens makes your property a less attractive lawsuit target. |

Timing is everything | Asset protection structures must be in place before any legal threat arises to avoid fraudulent conveyance rulings. |

Operational gaps create real exposure | Property manager fraud and rent delays are overlooked risks that can undermine even the strongest legal structure. |

Rental property asset protection explained: the insurance foundation

Most investors treat insurance as a checkbox. It is actually your first and most immediate financial shield. The critical distinction to understand is that a standard homeowner’s policy does not cover rental activity. The moment you place a tenant in a property, you need landlord insurance.

Landlord insurance covers three core areas: physical property damage, liability claims from injuries on the property, and loss of rental income when a covered event makes the unit uninhabitable. That last piece matters more than most landlords realize. If a fire forces your tenant out for three months, you still have a mortgage to pay. Without rental income coverage, that gap comes out of your pocket.

Here is where landlords commonly go wrong with investment property insurance:

Carrying liability limits that are too low. A $300,000 liability limit sounds like a lot until you face a serious injury claim with medical costs, lost wages, and legal fees stacked against you.

Failing to match the named insured on the policy to the legal owner of the property. If your LLC owns the building but the policy names you personally, claims can be denied outright.

Skipping umbrella policies. An umbrella policy extends your liability coverage beyond your base policy, typically from $1 million to $10 million, at a relatively low annual cost.

Landlord liability coverage and umbrella policies address different risk magnitudes. Think of your landlord policy as covering everyday claims and your umbrella as the backstop for catastrophic ones. You want both.

Pro Tip: Require your tenants to carry renters insurance as a lease condition. Tenant renters insurance covers their belongings and personal liability, which reduces the chance they file a claim against your policy for incidents that are actually their own responsibility.

Legal entity structures: LLCs and trusts

Insurance pays claims. Legal structures contain them. That distinction is the core of why insurance and entity structures address fundamentally different risks and why you need both.

An LLC, when properly formed and maintained, creates a legal wall between your personal assets and the assets held inside the entity. A lawsuit against the LLC targets only what the LLC owns. Your personal bank accounts, your primary residence, and your other investments sit outside that wall.

The problem is that wall is only as strong as how you treat it. Courts can pierce the LLC veil when owners commingle personal and business funds, fail to hold required meetings, skip annual filings, or operate the LLC as a personal extension rather than a separate entity. Proper LLC maintenance is not optional. It is the entire point.

Here is a comparison of the most common legal structures landlords use:

Structure | Primary benefit | Key limitation |

Single-member LLC | Liability separation per property | Requires strict formality to avoid veil piercing |

Series LLC | Multiple properties under one umbrella | Not recognized in all states |

Land trust | Privacy of ownership | Does not provide liability protection on its own |

Irrevocable APT | Strong creditor protection | Complex, costly, and difficult to modify |

Many experienced investors layer these structures. A property might sit inside a land trust for privacy, with the beneficial interest held by an LLC for liability protection. The land trust keeps your name off public records. The LLC keeps your personal assets out of reach. Neither alone is as effective as both together.

Pro Tip: If you own multiple rental properties, consider placing each one in a separate LLC. That way, a lawsuit targeting one property cannot reach the equity in your other holdings.

Financial strategies: equity positioning and creditor deterrence

Here is a concept most landlords never consider. Creditors and plaintiffs are rational actors. They pursue assets that are worth pursuing. If your property has $300,000 in exposed equity, it is a target. If it has $20,000 in exposed equity because the rest is encumbered by a mortgage or HELOC, it becomes far less attractive.

This is the logic behind equity stripping as a property protection strategy. By placing legitimate debt against a property, you reduce the net equity a creditor could actually collect. Senior liens get paid first in any forced sale, which means a creditor standing behind those liens may collect little or nothing.

There are a few critical points to understand before pursuing this approach:

Mortgages and HELOCs are the most common tools. Borrowing against your property’s equity and deploying those funds into other investments creates a lien that protects the remaining equity.

Cross-collateralization ties multiple properties together through shared lending arrangements, which can reduce exposed equity across your portfolio simultaneously.

Friendly liens, where a related entity holds a lien against your property, are a more advanced tactic that requires careful legal structuring to withstand scrutiny.

Timing is critical. Transferring equity or creating liens after a lawsuit is filed or threatened can be reversed by courts as fraudulent conveyance. These strategies must be in place before any legal trouble begins.

Think of equity positioning as making your property look like a poor target on paper. It does not eliminate risk, but it significantly reduces the incentive for a plaintiff to pursue you aggressively.

Operational risk management: property managers and intermediaries

Legal structures and insurance get most of the attention in asset protection conversations. Operational risks get almost none. That gap is where landlords actually get hurt.

When you hire a property manager or use any intermediary to collect rent and manage tenant relationships, you introduce a new category of exposure. Rental income delays of 5 to 8 months have been documented in cases where property managers failed to remit funds or where tenants were defrauded by individuals posing as property owners. These are not rare edge cases. They happen to landlords who did not have the right controls in place.

Protecting rental income at the operational level means treating your property management relationship like a business contract, because it is one. Here is what that looks like in practice:

Require a written management agreement that specifies exact remittance timelines, dispute resolution procedures, and your right to audit all financial records.

Set up direct deposit arrangements where rent flows into an account you control, rather than pooling through the manager’s operating account.

Conduct quarterly reviews of rent rolls, maintenance invoices, and tenant communication logs to catch discrepancies early.

Verify that your property manager carries their own errors and omissions insurance, so you have recourse if their negligence causes you financial harm.

Understanding how to protect cash flow from operational breakdowns is just as important as any legal structure. An LLC does nothing to recover three months of stolen rent.

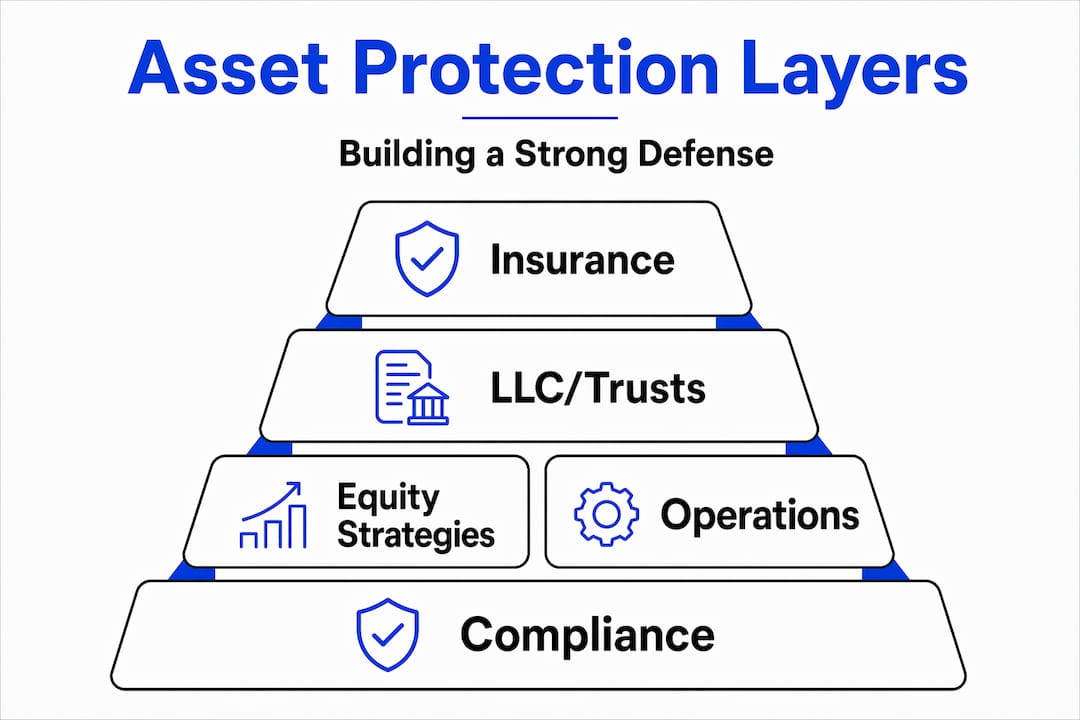

Putting it all together: a coordinated protection system

No single layer is enough. That is the most important takeaway from any serious look at rental property risk management. Landlords who rely only on insurance are exposed when claims exceed policy limits. Those who rely only on an LLC are exposed when they fail to maintain it. Those who rely only on equity stripping are exposed when the timing is wrong or the structure is challenged.

A complete asset protection strategy combines all of the following layers working together:

Layer | Role | Key requirement |

Landlord insurance | First-dollar claim payment and defense | Match named insured to legal owner |

Umbrella policy | Catastrophic liability backstop | Coordinate limits with base policy |

LLC structure | Contain liability to specific assets | Maintain formalities and separate finances |

Land trust | Privacy of ownership | Pair with LLC for full protection |

Equity positioning | Deter creditors by reducing exposed equity | Implement before any legal threat |

Operational controls | Protect rental income from intermediary risk | Written agreements and regular audits |

Compliance and record keeping tie all of these layers together. Your operating agreement must be current. Your annual filings must be complete. Your insurance policies must reflect the correct ownership entities. A mismatch anywhere in that chain creates a gap that a plaintiff’s attorney will find.

Pro Tip: Schedule an annual asset protection review with your attorney and insurance broker together. Many coordination failures happen because these two advisors never speak to each other about your specific structure.

Best practices for asset protection also include planning before you need it. Once a claim is filed or even threatened, your options narrow dramatically. Asset protection must be established before any known legal action to avoid having transfers reversed by courts.

My honest take on what landlords get wrong

I’ve seen landlords with strong insurance policies lose cases because their LLC was treated like a personal checking account. I’ve seen others with airtight legal structures get blindsided by a property manager who held their rent for six months. The pattern is always the same: one layer was treated as the whole system.

What I’ve learned is that most landlords underestimate coordination risk. It is not enough to have the right tools. They have to work together. Your insurance policy needs to name the correct entity. Your LLC needs to be funded and maintained properly. Your property manager needs a contract that protects your income, not just their fees.

The uncomfortable truth is that operational risks, specifically the ones introduced by property managers and intermediaries, are where I see the most real-world damage. These situations rarely make it into legal textbooks, but they drain cash flow and create liability exposure that no LLC can fix after the fact.

What actually works is treating asset protection as an ongoing system rather than a one-time setup. That means annual reviews, matched documentation, and advisors who understand how all the pieces interact. The landlords I’ve seen weather serious legal challenges are not the ones with the most complex structures. They are the ones who maintained their structures consistently and caught problems before they escalated.

— Main

How 2ndstreetpropertymanagement supports your protection strategy

Protecting your rental assets starts with sound legal and insurance structures, but it does not end there. Operational exposure is where many landlords lose ground, and that is exactly where professional property management makes a measurable difference. 2ndstreetpropertymanagement was built by investors who understand that protecting rental income requires more than paperwork. It requires consistent execution at the property level.

From written lease agreements and verified tenant screening to transparent financial reporting and timely rent remittance, the right management partner reduces the day-to-day risks that legal structures alone cannot address. If you want to see how professional property management can reduce your operational exposure and support your broader asset protection goals, explore what 2ndstreetpropertymanagement offers at 2ndstreetpropertymanagement.com.

FAQ

What does rental property asset protection actually cover?

Rental property asset protection covers the combination of insurance, legal structures, financial strategies, and operational controls that shield your properties and personal wealth from lawsuits, creditor claims, and income loss. No single tool covers everything on its own.

Is an LLC enough to protect my rental properties?

An LLC limits liability to the assets held inside it, but only if you maintain it properly with separate finances, annual filings, and documented formalities. A neglected LLC can be pierced by courts, removing that protection entirely.

What is the difference between landlord insurance and a homeowner’s policy?

Landlord insurance covers rental-specific risks including property damage, liability claims from tenants or guests, and loss of rental income. A standard homeowner’s policy typically excludes all of these once the property is used as a rental.

When should I set up asset protection for my rental properties?

Asset protection structures must be in place before any legal threat or claim arises. Transfers or liens created after litigation begins can be reversed by courts as fraudulent conveyance, which eliminates the protection entirely.

How does requiring renters insurance reduce my liability as a landlord?

When tenants carry their own renters insurance, their policy covers their belongings and personal liability first. This reduces the likelihood that tenant-related incidents result in claims against your landlord policy, helping preserve your coverage limits for more serious events.

Recommended

Rental Property Risks: Section 8 Gone Wrong and How to Protect Your Investments

Rental Property Risks: Section 8 Gone Wrong and How to Protect Your Investments

Comprehensive Property Management Solutions for Rental Property Owners

Rental Property Taxes Done Right vs Done Wrong: The Real Tax Advantages (and How to Use Them)

Comments