Financial Strategy for Landlords: A 2026 Guide

- Rey Rey Rodriguez

- 1 hour ago

- 8 min read

A financial strategy is the deliberate plan landlords and real estate investors use to manage income, control expenses, and make informed investment decisions to maximize returns and sustain growth. Unlike a simple budget, a true financial strategy integrates cash flow management, tax planning, debt ratios, and long-term investment goals into one coordinated system. For landlords, this means treating your rental portfolio like a commercial operation, not a side income stream. The team at 2ndstreetpropertymanagement works with investors daily and sees the same pattern: those who build a clear financial plan outperform those who react to problems as they arise.

What is a financial strategy for landlords?

A landlord’s financial strategy must function as a commercial system that links cash flow, tax liabilities, and debt-to-asset ratios to support portfolio growth. Many investors confuse movement with progress. Collecting rent every month feels like success, but without a plan connecting that income to expenses, reserves, and reinvestment, you can show a profit on paper while running out of cash in practice. This is the liquidity trap that experts identify as one of the most common reasons real estate investors stall.

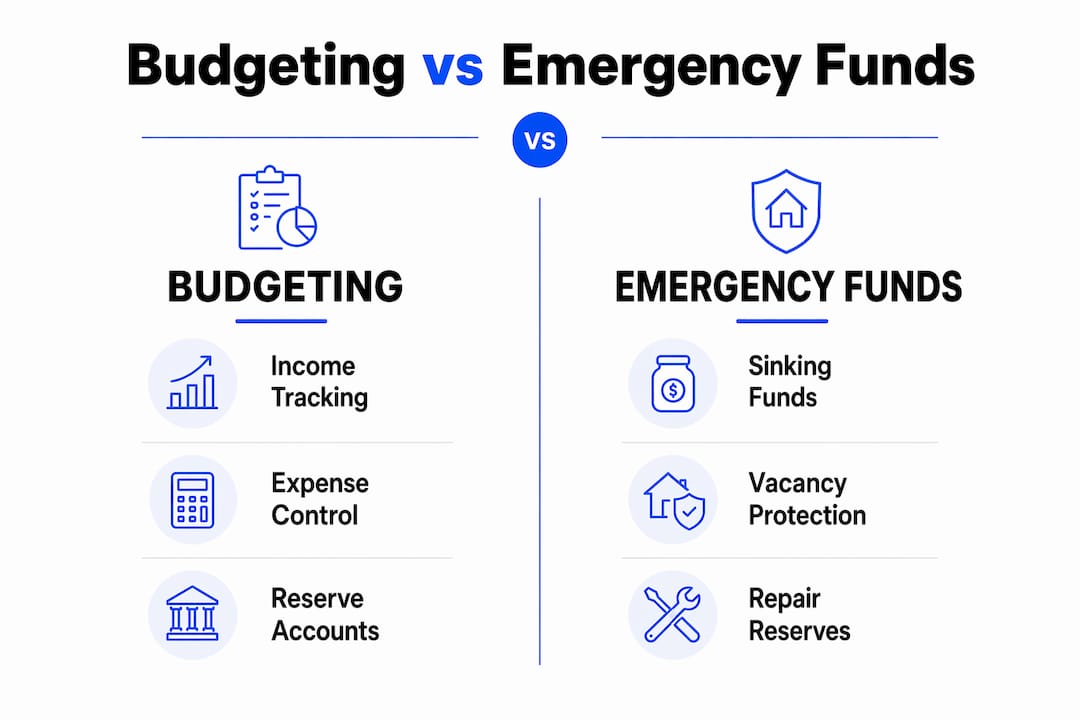

The core components of a sound investment plan for landlords include four pillars: income tracking, expense control, emergency reserves, and long-term capital allocation. Each pillar depends on the others. Strong rental income means nothing if repairs drain your reserves. Low expenses mean nothing if you have no reinvestment plan. A financial strategy ties all four together into a system that runs consistently, regardless of market conditions.

How should landlords structure budgeting and expense management?

Budgeting is the foundation of any personal finance strategy, and for landlords it requires more precision than a standard household budget. Fidelity’s budgeting guideline recommends allocating 60% of income to essential expenses, 30% to discretionary spending, 10% to debt repayment, and 15% to retirement contributions. Adapted for rental income, this framework helps you separate operating costs from growth capital and avoid spending tomorrow’s repair fund today.

Common landlord expenses to budget for include:

Mortgage payments and property taxes

Insurance premiums (property, liability, and loss of rent)

Routine maintenance and landscaping

Property management fees

Vacancy allowance (typically budgeted as a percentage of annual rent)

Capital expenditure reserves for roofs, HVAC systems, and appliances

Accounting and legal fees

One trap many landlords fall into is lifestyle inflation during high-occupancy periods. When every unit is rented and cash flow is strong, it is tempting to increase personal spending or delay building reserves. That decision consistently creates problems when a vacancy or major repair hits. Discipline during good months is what funds stability during difficult ones.

Pro Tip: Separate your rental income into at least two accounts: one for operating expenses and one for reserves. This single habit prevents you from accidentally spending repair funds on day-to-day costs.

What emergency fund strategies protect landlords from vacancy and repair risks?

An emergency fund is not optional for landlords. It is the buffer that keeps a vacancy or a failed water heater from becoming a financial crisis. Experian and Fidelity recommend maintaining three to six months of essential expenses in liquid savings, with an initial milestone of $1,000 set aside immediately. That first $1,000 matters because it breaks the inertia of starting.

Build your emergency fund using this sequence:

Set aside $1,000 immediately from your next rental deposit or income cycle.

Calculate three months of essential property expenses, including mortgage, insurance, and utilities.

Automate a fixed monthly transfer from your operating account to your reserve account.

Once you reach three months, extend the target to six months as your portfolio grows.

Replenish the fund within 90 days any time you draw from it.

Beyond a general emergency fund, landlords benefit from segregated sinking funds for specific capital expenditures. A sinking fund is a dedicated account where you deposit a fixed amount monthly toward a known future expense, such as a roof replacement or HVAC upgrade. This approach removes the shock of large repair bills and eliminates the need to put emergency costs on credit.

Pro Tip: Name your sinking fund accounts by property address and expense type, for example “123 Main St. Roof Fund.” Specificity makes it harder to raid the account for unrelated expenses.

How can landlords create a long-term financial plan to grow their portfolio?

A long-term financial plan operates on a 3 to 5-year horizon, which is fundamentally different from an annual budget. Your budget controls day-to-day operations. Your strategy governs refinancing decisions, property acquisitions, asset liquidation, and retirement savings. Treating them as the same document is a mistake that keeps many landlords stuck at one or two properties.

Setting investment goals that drive decisions

Your long-term goals should be specific and tied to numbers. “Grow my portfolio” is not a goal. “Acquire one additional property by the end of 2027 using a cash-out refinance on my current property” is a goal. Goals at this level of specificity force you to track the metrics that matter: equity position, debt service coverage ratio, and available capital.

Fidelity’s 2026 guidance highlights that increasing your savings rate by just 1% compounds meaningfully over time. For a landlord reinvesting rental income, that principle applies directly. Directing an extra 1% of gross rental income into a retirement account or property acquisition fund each year creates a compounding effect that accelerates portfolio growth without requiring a major lifestyle change.

Asset allocation and reinvestment principles

A sound long-term plan addresses how you allocate capital across your portfolio. Key decisions include:

What percentage of net income goes toward debt paydown versus new acquisitions?

Do you prioritize appreciation markets or cash flow markets for your next purchase?

How does depreciation factor into your tax strategy each year?

At what equity threshold do you refinance to pull capital for reinvestment?

Automation plays a critical role here. Setting up automatic transfers to retirement accounts and reserve funds removes the decision from your monthly routine. When savings happen automatically, you stop negotiating with yourself about whether to save this month.

Annual reviews of your financial plan against current interest rates and market conditions keep your strategy current. A plan built in a 3% rate environment needs adjustment in a 7% rate environment. Reviewing annually is not optional. It is the mechanism that keeps your strategy connected to reality.

Planning Element | Annual Budget | 3–5 Year Strategy |

Focus | Day-to-day cash flow | Portfolio growth and capital allocation |

Key metrics | Monthly income vs. expenses | Equity, debt coverage, ROI |

Decision type | Maintenance, rent adjustments | Acquisitions, refinancing, retirement |

Review frequency | Monthly | Annually |

What financial management systems help landlords stay disciplined?

A financial command center is the concept of linking all key metrics, including cash flow, debt ratios, tax liabilities, and investment performance, into one dashboard you review regularly. Without this, landlords manage reactively, addressing problems only after they become urgent. Automation reduces the psychological burden of managing multiple properties by creating systems that run in the background without requiring constant decisions.

Practical systems for small to mid-size landlords include:

Automated rent collection through a dedicated property management platform

Scheduled monthly transfers to reserve and retirement accounts

A shared spreadsheet or property management software tracking income, expenses, and vacancy rates by unit

Quarterly tax estimates calculated and set aside automatically

Annual depreciation schedules reviewed with a CPA each year

The most common pitfall is reactive management. Landlords who wait for problems to appear before addressing finances consistently underperform those who build proactive cash flow systems. Neglecting reserves is the second most common mistake. A property that generates $1,500 per month in net rent but has no capital expenditure reserve is not a cash-flowing asset. It is a liability waiting for a repair bill.

Pro Tip: Schedule a 30-minute financial review on the first Monday of each month. Review rent collected, expenses paid, and reserve balances. This single habit catches problems before they compound.

Key takeaways

A landlord’s financial strategy works when it integrates budgeting, emergency reserves, and long-term investment planning into one coordinated system reviewed annually.

Point | Details |

Budgeting framework | Apply the 60/30/10+15 rule to separate operating costs from reserves and retirement savings. |

Emergency fund target | Maintain 3–6 months of essential expenses in liquid savings, starting with $1,000 immediately. |

Sinking funds by property | Use segregated accounts for capital expenditures to avoid drawing from personal income. |

Long-term planning horizon | Build a 3–5 year strategy that governs acquisitions, refinancing, and retirement contributions. |

Automation as discipline | Automate savings and transfers to remove monthly decisions and maintain consistency. |

The discipline gap most landlords never close

Most landlords I work with understand the theory. They know they should have reserves. They know they should plan beyond the next lease renewal. The gap is not knowledge. It is execution under pressure.

When a tenant leaves unexpectedly or a repair bill arrives in the same month as a property tax payment, the investor without a system scrambles. The investor with a system writes a check from the sinking fund and moves on. That difference compounds over years into a portfolio gap that is nearly impossible to close later.

The other pattern I see consistently is underestimating the difference between profit and cash flow. A property can show positive returns on paper through appreciation and depreciation while generating negative monthly cash flow. Investors who track only ROI miss this. Real estate investment returns require you to track both simultaneously.

Pre-commitment is the most underrated tool in investment planning. Writing down your acquisition criteria, your reserve targets, and your savings rate before the market gets volatile keeps you from making emotion-driven decisions when conditions shift. The plan you build in a calm moment is almost always better than the decision you make under pressure.

— Main

How 2ndstreetpropertymanagement helps you build a stronger financial plan

2ndstreetpropertymanagement was built by investors for investors, which means the team understands the gap between theory and what actually works across a real portfolio.

Whether you are managing your first rental or scaling a multi-property portfolio, 2ndstreetpropertymanagement offers tailored investment solutions that connect financial planning with day-to-day property operations. From expense tracking to vacancy management, the goal is to give you the systems and support that keep your portfolio performing through every market cycle. Reach out to 2ndstreetpropertymanagement to discuss how a structured financial approach can work for your specific portfolio and goals.

FAQ

What is a financial strategy for real estate investors?

A financial strategy is a coordinated plan that links rental income, expenses, reserves, and long-term investment goals into one system. It goes beyond budgeting to include tax planning, debt management, and portfolio growth decisions.

How much should landlords keep in an emergency fund?

Landlords should maintain three to six months of essential property expenses in liquid savings, with a starting milestone of $1,000 set aside immediately, per Fidelity and Experian guidance.

What is the difference between a budget and a long-term financial plan?

A budget controls day-to-day income and expenses on an annual cycle. A long-term financial plan operates on a 3–5 year horizon and governs decisions like property acquisitions, refinancing, and retirement contributions.

How does automation help landlords manage finances?

Automation removes monthly decisions by scheduling transfers to reserve accounts, retirement funds, and tax savings. Bread Financial research confirms this reduces the psychological burden of managing multiple properties.

What is a sinking fund and why do landlords need one?

A sinking fund is a dedicated savings account where you deposit a fixed monthly amount toward a known future expense, such as a roof or HVAC replacement. It prevents large repair costs from disrupting cash flow or requiring credit.

Recommended

Comments